To survive a business, funds are an essential need of any business. In recent years, small and medium-sized enterprises have witnessed vast growth.

With a high volume of emerging small and medium businesses are bringing new strategies, innovation into the market, and to help them in fueling their growth, various banks, NBFCs, and other financial institutions have initiated several customized loan schemes to cater business needs.

Whether you are a startup or a business that has been in the market for years, the need for funds to operate any business is common.

Though business loans are mostly secured and are backed by collateral. But have you ever heard about unsecured business loans? Most of you may know and some of you may be unclear about the term unsecured.

Unsecured business loans refer to those credit facility that allows you to avail a loan without the need for collateral.

Most of the banks, Non-Banking Finance Companies (NBFCs), and financial institutions provide this type of loan to borrowers without asking for security. With a small business loan, one can develop their business in many ways.

If you are looking for an Unsecured Business Loan to grow your business, you have come to the right place. In this article, we would learn “How to Grow SME businesses with unsecured business loans”.

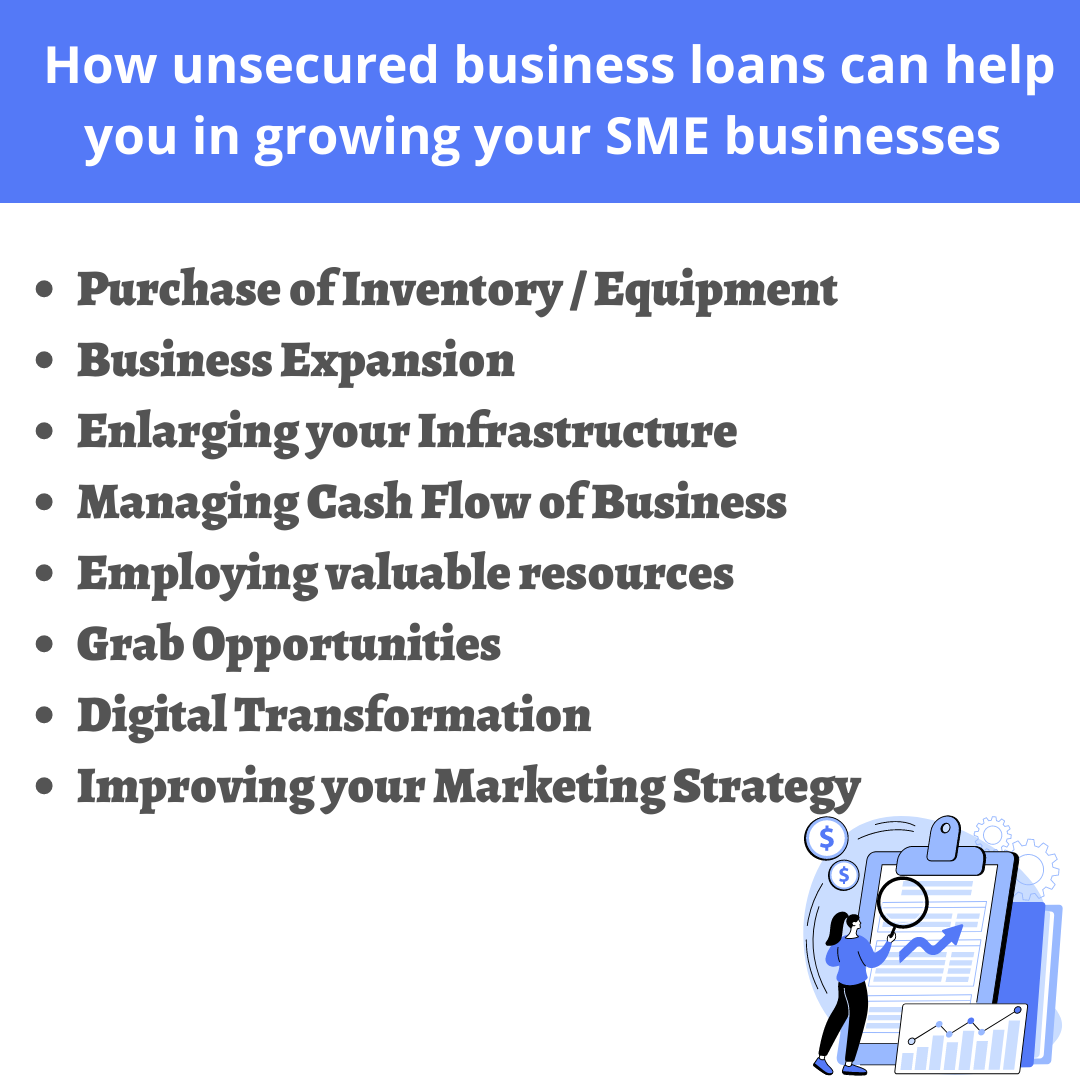

Table of Contents: How unsecured business loans can help you in growing your SME businesses Why Unsecured Business Loan is a Better Option for Small Businesses? Things to Know Before Taking an Unsecured Business Loan Who can get a Business Loan? How to Ensure Your Loan Gets Approved? Top Mistakes to Avoid When Availing a Business Loan How to Apply for a Small Business Loan Online? To sum up |

Inventory and Equipment are a basic requirements of every business operation. In a highly competitive global marketplace, a good inventory system is important for business sustainability and growth.

The need for equipment and inventory can arrive at any time in business. But, delaying them can affect your business wisely. Hence, opting for an unsecured loan proves to be beneficial in managing your business.

Sufficient inventory will ensure that your business functions are hassle-free. The loan comes with flexible tenure which makes it easier for you to repay the borrowed amount at your convenience.

All successful businesses or startups ultimately face the problem of managing business expansion or development. Business expansion is where the business reaches the point of growth and seeks out additional options to generate more profit.

As a business owner, you will seek funding when you feel this is the right time to expand your venture.

With an unsecured business loan, it becomes easier to move your small-sized office to a bigger one, open a new branch, purchase required inventory, hire more staff, and so on. Thus, business expansion are possible by taking care of a little bit of everything.

For any company infrastructure is the key foundation and it’s the basic structure that all companies are built on. Good infrastructure is vital for the functioning of a business.

A good infrastructure is called when there is a proper office space, storehouse, or a place where inventory can be kept off. Employees always prefer to work in a good environment, a company with a great infrastructure is enough to attract clients and employees.

Availing of an unsecured business loan can help you in building and improving your business infrastructure.

Most of the entrepreneurs lack the vision to think outside of the box and fail to implement business strategies to improve the cash flow in their business.

An improved cash flow reflects a positive image of any business's success. But unfortunately, this cash flow cannot be achieved by a simple producing and selling approach. As a business owner, you should think of different ways to make your business financially stronger so that there won’t be any effect on cash flow.

In order to maintain a smooth cash flow for business operations including inventory purchases, staff salaries, transportation facility, and office rent, paying off taxes might fall due to a shortage of funds. In such a scenario, a small business loans come into the picture, as availing of them can help you meet your requirements. Further, loans can be repaid by the profit generated from the investment.

Generally, small and medium-sized enterprises at their initial stage face employment-related complications. The success behind most of the companies is their employee's teamwork.

When it comes to expanding your existing business, you will often need more resources and employees are the most valuable assets of any company.

As a result, employing highly qualified and skilled staff will ensure that your company is functioning smoothly.

A Business Loan will increase your company’s capacity to hire more quality people and ultimately increase productivity and get more work done.

Every business has its own seasonal and customer demands, grabbing opportunities always shows to be beneficial and profitable. Being a business owner, you must be fully prepared to grab the opportunities.

Circumstances such as the absence of funds are the biggest obstacle that might come to your path. In such cases, you shouldn’t fall short of funds. An unsecured loan keeps you one step ready and helps you in achieving the milestones of success.

One of the significant benefits of such a loan is that you don’t have to risk ownership of any of your belongings by submitting them as collateral.

Digital transformation changes the way an organization operates, and a Business needs its business into a digital one.

A new product on the market will not reach customers until it gets advertised through digital platforms. Often, advertising costs huge expenses, but eventually it can be repaid off over a short period.

This is one of the smartest ways to grow your business by fulfilling the demand of your customers. As a result, you would be able to reach more customers.

To have your business presence digitally, you should have certain resources and funds. Hosting and maintaining an online website requires money. To do so, you need a team of digital marketers, either you can hire them in-house or get help from external digital marketing agencies.

Therefore, you need to invest your money as well as time in developing an eye-catching and useful website that should attract the customer at first sight. As compared to traditional (offline marketing), online marketing proves to be more beneficial. This means it is comparatively cheaper and investing in such marketing will give a host of benefits.

In case you don’t have enough funds, opting for a small business loan or unsecured business loan can help you fund all this.

Learning about, and focusing on, improving marketing operations is becoming more challenging in today’s world. You might develop an attractive website, but if you don’t know how to market it in the right way, you may face a loss by leaving your customer to some other competitor.

Whether you are promoting your website through online or offline, a keen marketing analyst requires you to study the market, do research work, make documentation, and then use the findings to attract the right audience.

However, understanding your customers, implementing certain plans and measuring campaign performance are all the key steps in building an apt marketing strategy.

All this requires money because you need a team of well-qualified and skilled staff to promote your organization and make it a well-known brand. Thus, obtaining an unsecured business loan will help in achieving your goals.

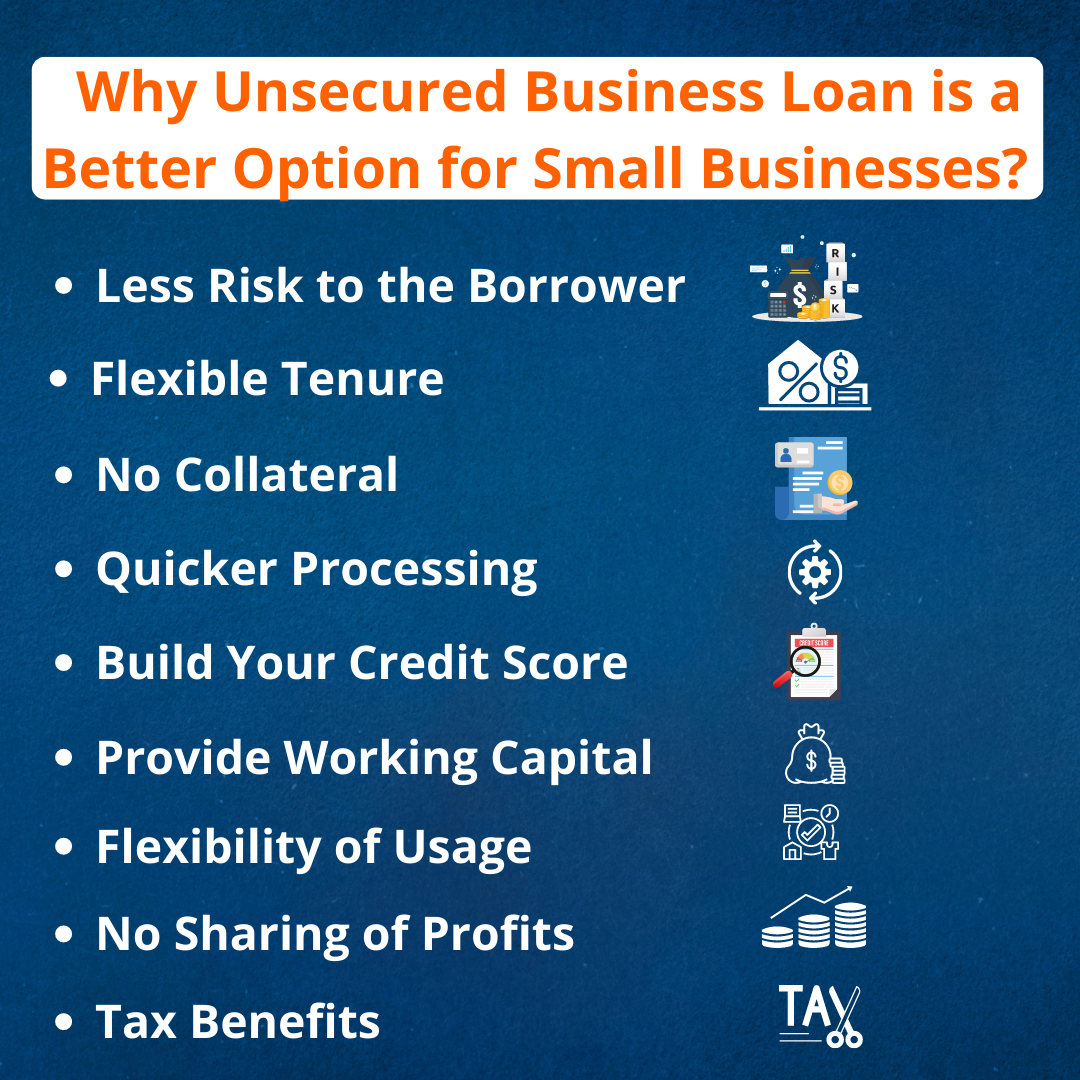

Most of the small businesses prefer unsecured business loans because they do not want to risk their property, vehicle, or any other asset as a security. From the business owner's point of view, unsecured small business loans are considered safer and more convenient compared to secured loans.

The main difference between a secured and an unsecured business loan is the collateral. In secured business loans, borrowers are required to pledge their assets as security, which means it is a less risky profile from the lender's perspective.

Whereas unsecured business loans do not require borrowers to pledge any kind of collateral as security, which means if the borrower defaults on the loan, their personal or business assets will not be at risk.

As per the current scenario, most startups do not have assets to pledge as security. Hence, they can make use of unsecured loans to fund their business needs.

This type of credit facility comes with a flexible repayment tenure option. Typically, the loan is available for a short duration. The repayment term ranges from 12 and 36 months from banks and financial institutions.

The flexible tenure aids business owners to pay off their outstanding balance in a short period while keeping their budget intact. The shorter and flexible loan tenure allows borrowers to maintain positive cash flow.

As the term itself suggests, these business loans are unsecured in nature. In which you do not have to provide collateral against availing of the loan.

Obviously, this is the biggest advantage for you. As a business owner, you don’t have to risk your property, vehicle, or any other asset to raise funds. In such a case, a small business loan without collateral is a very advantageous feature for small or medium business owners.

You can start earning better and begin to repay the loan amount easily. When you take an unsecured loan no mortgage is payable, which means that there is no risk of losing the assets.

This feature is especially beneficial for those businesses that are just starting up and don’t have any assets or securities to provide as collateral. Thus, availing unsecured business finance becomes much more feasible for business owners or entrepreneurs that are just starting their business ventures.

In secured loans, the disbursement process usually takes a longer time because the lenders must assess the borrower profile in detailed aspects such as nature of business, financial record, credit history, other financial obligations, and so on.

In addition, the lenders have to study the property papers and conduct evaluations to determine the actual market value of the collateral, depending on the value of collateral; the maximum loan amount is granted. Hence, the process is lengthy and time-consuming. Whereas the turnaround time of an unsecured business loan is quick and easier.

Most borrowers are unaware of the benefits of a small business loan in enhancing their credit score. However, this funding facility comes with short tenure, making it easier for business owners to repay the loan conveniently.

Repaying the loan on or before due date not only helps in avoiding unwanted penalties but also aids in building your credit score that will ultimately prove to be beneficial in securing a loan at better interest rates and qualifying for simplified loan terms.

A liquidity crisis is one of the key business challenges faced by small business owners. To run your business operations smoothly, businesses require funds to cover their working capital requirements.

Having adequate working capital can assist enterprises in meeting varied needs such as creditor liabilities, utility bill expenses, inventory purchases, and so on. This is where an unsecured short-term loan for small businesses comes in handy.

For any business, the need for funds is never-ending. You never know when or for what situation your business will need money. Be it immediate funds required to meet up overhead expenses, purchase machinery, pay utility bills, or anything else. With an unsecured small business loan, you can get the flexibility of usage to great extent.

Most lenders don’t even ask about the business plans for the funds. All you have to do is compare and choose the right lenders and check your eligibility with them, complete the application form with all required documentation, and receive the funds in your account.

This has been seen that many small businesses avail alternate financing from angel investors or venture capitalists to set up or expand their business. But convincing such investors to invest in any business venture is a complicated task.

Moreover, approaching these venture capitalists without a proper detailed business plan can lead to the rejection of proposals. Also, many angel investors ask to share the company’s profits in return for their investments. Often, the company owners lose their own sole ownership of the company in the process of availing funds without incurring any debt.

As compared to banks or non-banking financial companies (NBFCs) it is a lot more convenient and easier to obtain small business loans. The awesome part is that as a business owner you do not need to risk anything, neither your assets nor stake in the business.

The best part is whatever profit a business makes with the use of a business loan is solely for the business owner to enjoy. The owner need not share any part of his/her business profit with the lender or someone else.

It may sound weird, but it exists an unsecured business loan come with tax benefits.

The interest that you would be paying during the loan repayment is subject to a tax deduction.

The amount paid back to the lending institutions in the form of interest is tax-deductible. A tax deduction in the finance industry is known as a deduction that lowers an individual’s tax liability by lowering their taxable income.

Borrowers can benefit from a business loan by deducting their interest amount from the business expenditure to come at the taxable amount.

Thus, it is an effective tool for Micro, Small and Medium Enterprises (MSMEs) to lower their tax liability and use the funds for expanding their business. In order to qualify for these benefits, one should include the interest payment in their book’s expenditure column.

Get Unsecured Business Loan @ Low Rates

Also Read: Tax Benefits on Business Loan in India

For businesspeople, one of the worrying areas for growth is the everlasting prospect for sources of working capital. If you run a small and medium-sized enterprise (MSMEs) with relatively limited business assets or collateral, finding ways to raise funds can be burdensome.

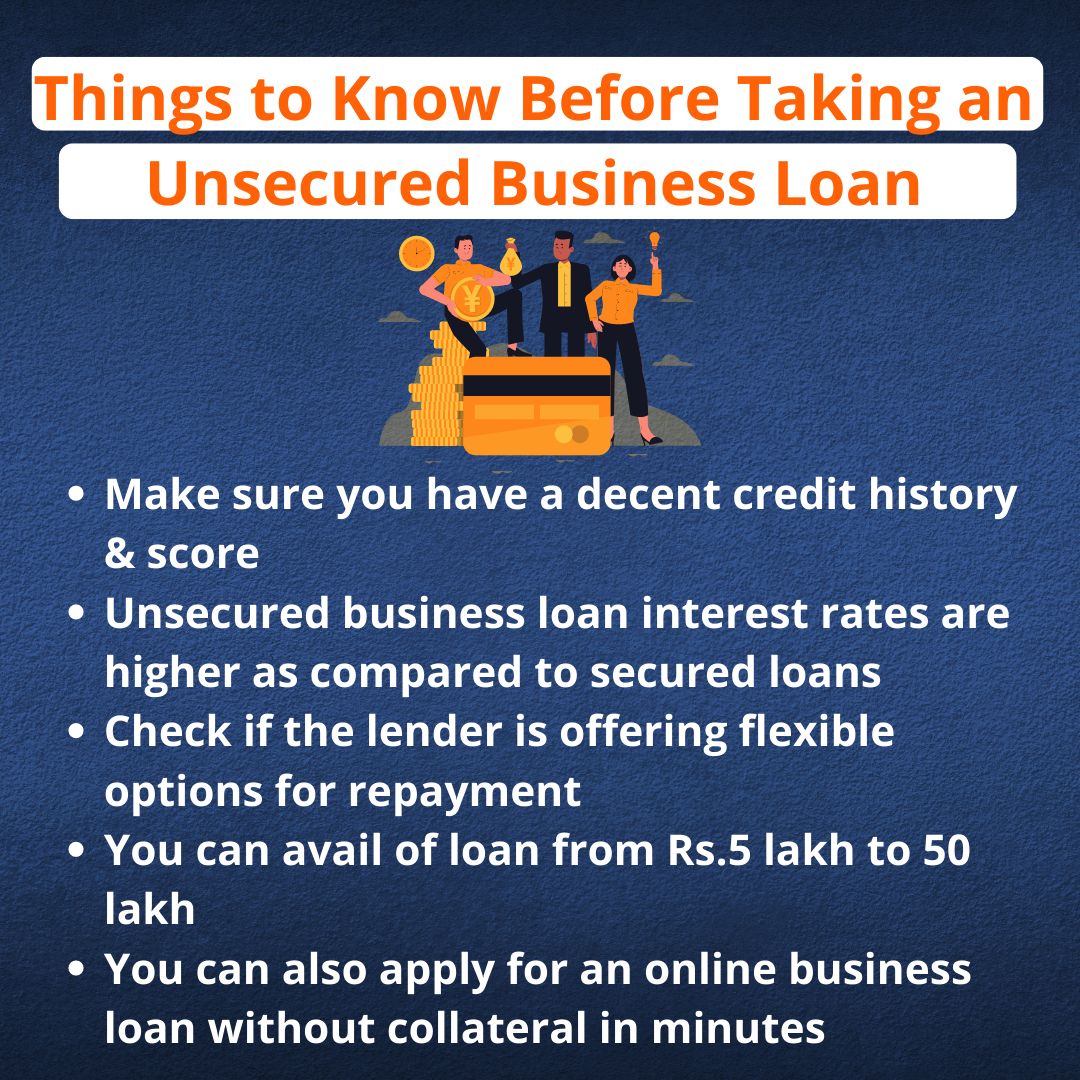

To improve your chances of getting a business loan from a bank or financial institution, here are some things that you should know before applying to the lender.

The first step is to check whether your profile comes under the eligible entities category. The following are the list of eligible entities:

These are the general loan eligibility criteria to keep in mind to make the process seamless:

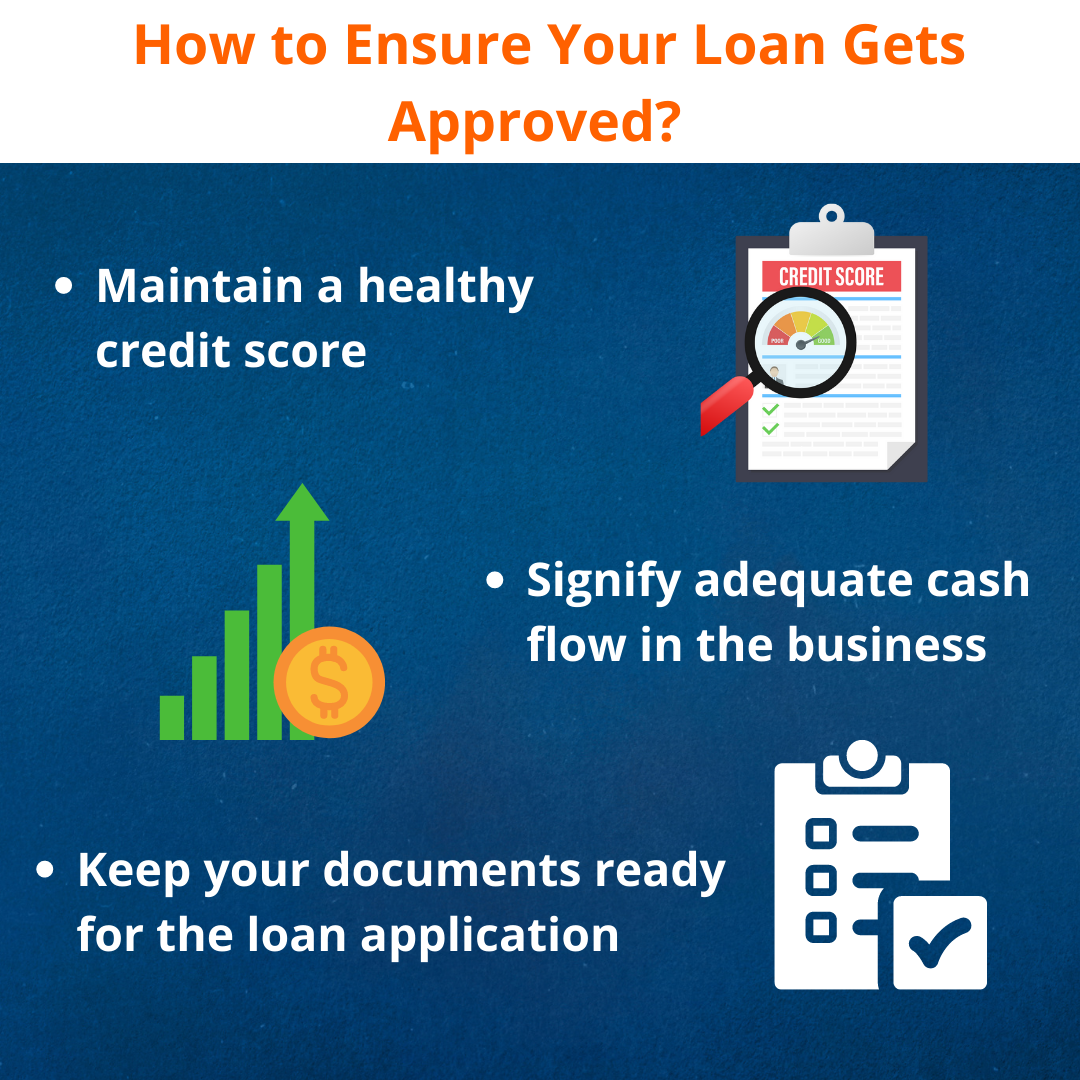

Qualifying for a business loan means you are successfully exhibiting your repayment capability. Below are some ways in which you can demonstrate your ability.

Lenders always check the credit score of both individual and businesses to assess their creditworthiness.

Most of you might have questions about how an individual's credit scores can affect business eligibility. Then yes, what you guess is right; as a business owner or founder, your personal credit score which includes the record of payment history are considered to know whether you are good at repaying bills/debts and maintaining financial records.

In case you were not, then the lender would consider your profile to be ineligible as you are doing a considerable contribution to business your business eligibility to gets unqualified. This is how an individual credit history significantly affects the eligibility for a business loan.

Hence, having a healthy credit score indicates that you are financially disciplined and are quite unlikely to default on repayment. Apart from that, it also reflects your capability to make wise financial decisions.

Despite the fact, that the minimum personal credit score required to qualify for a business loan depends on the lender. Usually, a credit score of 700 or above will enhance your credibility, and thereby loan worthiness.

Get Your Business Credit Report

Also Read: How to Improve Your CIBIL Credit Score

While deciding your eligibility for a small business loan, the lender will conduct a detailed investigation of your business cash flow which includes past and future projections to know whether it is capable of repaying the size of the loan that you are seeking.

Your previous tax returns and existing debts will also be taken into consideration to determine your repayment capability.

Hence, make sure you can signify appropriate cash flow so that the lender will find you as a potential borrower and an adequate cash flow will safeguard your assets.

To ensure your loan is approved, give equivalent importance to the documentation required for the loan application process.

To streamline the process, you should gather all the relevant documents as specified by the lender. However, you will have to submit a few of the following documents for verification:

There is no such easy road to success. Starting up and enhancing a successful business requires years of hard work and patience. To increase your business size, you might need capital at each stage of growth in your business.

Arranging working capital could be quite a difficult financial burden, especially if your company is to start and doesn’t have any external source of funds. That is where the business loan comes into the picture.

You can ensure approval for your business loan by avoiding some common mistakes. Let’s examine some of the common mistakes that you as a borrower should avoid:

A business plan/project report is one of the most essential documents requested by the lending institution while providing you with a credit facility. Before a lender agrees to offer you a loan for your business, it needs to be sure that your business plan is good enough to generate returns.

Usually, lenders want to know where you are going to utilize the borrowing loan amount and want to assess your ability to repay the loan within the specified time period.

With a solid business plan/project report, you can present exhaustive information about your business so that it can be approved at first sight itself.

While having a poorly written business plan or a nil business plan can lead to rejection. According to an entrepreneur's study, the majority of small business ventures do not have an appropriate business plan. If you understand the information a business plan is supposed to contain, it becomes difficult to imagine a business succeeding without one.

You must present a perfect business plan containing all the details. Your project report should include a detailed background and nature of your business, with a clear description of the ownership structure, management team, and details of their expertise. Additionally, you should also include sensible and considerable reasons for borrowing the funds along with the execution strategy.

The key principal aspect of a business plan that the lending institution are keen on is the financial aspect.

So, you should include details on how you plan to generate revenue and repay the loan within specified tenure periods.

Securing a business loan is not an easy task, especially if you are in the early-stage small business. Lenders always look for years of profitability or some guarantor or to have a stable balance sheet before granting a business loan. That’s where financial documents of your business play a critical role in securing a business loan.

It has been that most of the SMEs and MSMEs make mistakes such as misreporting their actual financial status. Depicting inflated income and reduced expenses can make the business look profitable but might get you into trouble, and you may end up facing rejection of your business loan application. So, never do that.

Therefore, keep your financial documents up to date and up-to-actual before approaching any lender. Ensure you need to fill in the details of assets, liabilities, income, and expenses of your business, along with your financial details in your loan application form.

Also, remember to provide accurate details of your business financials. As some lending institutions may ask for audited financial documents of your business such as cash flow statements, balance sheets, and profit and loss statements. Keep in mind that lenders prefer honesty not inflated financials.

There are plenty of loan product options available in the market for Micro, Small and Medium Enterprises (MSMEs).

Some of the most popular are startup loans, working capital loans, machinery loan, overdraft facility, equipment financing, invoice/bill discounting, loan against property and, letter of credit against collateral or in cases without collateral can also be availed.

The presence of many customized business loan products can confuse business owners a little bit and you may end up choosing the wrong product.

Therefore, you must conduct in-depth research and apply for the right product best suited to your needs. In case if you opt for an incorrect product, then your cost to change the product shall be higher than what you chose!

It is recommended to understand the lending options that are available and then go ahead further with the process of loan application.

To save yourself from choosing the wrong loan product and want to get a customized loan option. Visit Financeseva.com that have ample of loan options and a team of experts who suggest the right type of loan based on your business profile and specific requirements.

Many entrepreneurs and business owners proceed with the business loan application without completely understanding the requirements for the lending product. The eligibility criteria for a business loan are available on the lenders’ websites.

You should be completely aware of the eligibility criteria and understand if your business meets the requirements. However, it is also important to have a clear idea of the steps to obtain a loan in a disciplined manner.

When it comes to a business loans, the procedure can be lengthy; you will be asked to submit a list of documents as specified by the lender. Failing to submit all the supporting documentation can result in rejection or delay with your application.

To understand the procedure of obtaining a business loans. Financeseva will not only help you in proceeding with the application and make you beneficial of cost.

Also Read: Reasons Indian Businesses faces Rejection for Small Business Loans

Applicants can apply for a business loan by either visiting the bank or applying online through the banks or online marketplace official website. It is always recommended to apply online as it saves time, energy and cost. Apart from that, you can make the best use of online eligibility and EMI calculator tools to make an informed decision.

The detailed step-by-step guide for applying business loan through Financeseva is mentioned below:

Step 1- Visit Financeseva.com, Under MSME-wide categories you will find an unsecured loan, in which you have to click on “Business Loan”.

Step 2- In the enquiry form, you will be asked to share your personal details like name, email address, mobile number, state, city, and loan requirement details.

Step 3- After filling out the form, click on “Get a Free Call”. Our dedicated representative gets you in touch within 24 hours of receiving your request.

Step 3- We will verify all the eligibility details and guide you about the complete loan process and the required documentation.

Step 4- If you are eligible and interested, the representative will fix the appointment for document pick-up and further the loan process. However, nowadays some lenders are providing the flexibility of uploading documents online. In such cases, you will be asked to share the documents over email.

Step 5- Once your documents are verified, based on your credit score and eligibility, the bank will decide to sanction or reject your business loan application. If all seems good you get a sanction letter from the bank mentioning the key loan terms like business loan interest rate, processing fees, tenure, and prepayment charges.

Step 6- Finally, the desired loan amount will be credited to your registered bank account.

Apart from the above list, still there are other common mistakes which include not reading the loan agreement, quoting requests for multiple loans at a single time, and missing out on necessary business information may also result in delay or rejection of your business loan application.

Here are some important tips to secure your business loan without a hassle:

To wrap it up, be aware of the aspects that are considered by the lender while granting your business loan application and prevent yourself from making common avoidable mistakes.

With Financeseva, you can get customized loans for your small business and streamline your working capital requirement soon enough. Financeseva provides personalized and superfast services and helps applicants to get quick approval at attractive rates addressing their needs at the right time.

CA Vikas Jain - Our Mentor