Running a business in India is a very tough thing. The increasing competition in the market is lowering the profit margins and new business models are making it tough for small businesses to stay afloat. This makes the entrepreneurial journey multifaceted. One of the main concerns is being an entrepreneur is funding the ventures.

That’s where the small business loan comes into the picture, a small business loan are used to meet your business goals.

When it comes to loans and credit offers, the banks and other financial institutions become more cautious while granting loans and ask the borrower to meet certain eligibility criteria and follow the procedures in order to qualify for business loans.

Failing to fulfill the eligibility can lead to loan rejection and rejection is not accepted easily may be whatsoever the reason, situation or condition is. The moment you come to know that your business loan application is rejected, you are most likely to feel that results in dejection and disappointment.

Therefore, to avoid any loan application rejection, you can consider the following measures and suggestions:

The credit history of the company and its respective founders/directors play an important role in the loan approval process. When it comes to availing of a business loan, the company’s credit score matters a lot.

The CIBIL/Credit score reflects creditworthiness and indicates how well the company and its founders/directors maintained their financial activities, particularly the debts in the past.

In case the company has defaulted on its previous loans and the same will be reflected in the credit report and this will reduce the score eventually. Apart from this, the personal credit score also carries an equivalent weightage because if we think logically about an individual who cannot handle his/her personal score how can he/she manage the company’s credit score.

Hence, both the business credit and personal credit scores are equally considered by the lenders. A low credit rating increases the chances of loan rejection for business.

CIBIL score is a 3-digit-numeric that must be maintained above 700 out of 900 to get a business loan at low-interest rates. An applicant with a score of 650 or lower tends to face loan rejection.

Checking your CIBIL score and generating a credit report is absolutely free at financeseva.com. It’s an online process that takes less than 5 minutes to check, download your report and start maintaining a healthy CIBIL score to secure easy finance.

Also Read: How to Improve your CIBIL/Credit Score?

One of the most essential elements in your business loan application is an effective business plan/project report that needs to be submitted while applying for a business loan. The lender deeply assesses the business plan to check the potential growth of the organization and the feasibility of the business projections.

In case the lenders feel unsure about the business plan, and it would be a risky investment, you might receive a rejection for your loan application.

Therefore, it is important to project an effective business plan that must seem realistic and give enough confidence in your projections the major elements such as expected profit margins, target set of audience, and revenue generation should be given even more consideration in your business plan.

To avoid rejection, you must present a well-drafted business plan at the time of application submission. Make sure you consider the above-mentioned elements to boost the chances of loan approval.

Also Read: Project Report for Bank Loan to Boost Your New Business

Usually, a small business loan application is rejected because of incomplete documentation. Along with a loan application form, a complete set of documents are required to submit to the concerned bank as specified.

Documents include identity proof of individual, establishment proof, company bank statements, financial statements, personal and company tax returns, business plan, and other legal documents as requested by the lender.

It is often seen that borrowers submit the application with incomplete, missing, false or fake documents which end up getting their business loan application rejected.

Hence, check the lender’s document checklist before applying for a loan. Failing to do so will not only lead to rejection but also reduce your credit score.

Based on the business cash flow, the lender judges your repayment capabilities. Insufficient cash flow loses the bank’s trust in you which further results in loan rejection. Often small and new businesses face struggles with adequate cash flow, but this is not too consistent.

Cash flow can be maintained properly by arranging timely invoicing and removing unwanted or additional expenses. This enhances to sharpen the accounting as well as management skills in a better manner.

Secondly, not every bank offers unsecured business loans or collateral-free loans. In such cases, business owners and enterprises are required to pledge security against the loan amount.

Unable to submit collateral shall result in loan rejection. Residential or commercial properties including home, office, shop, godown, warehouse..etc.) are widely considered as a common type of collateral.

Also Read: How to Get a Startup Business Loan without Collateral?

The term “No Credit” refers as new to credit which means businesses or applicants do not have any current or previous credit usage in their credit history; their CIBIL Score will reflect Nil or Zero.

Borrowers who want to start their own business face some difficulties in the loan approval or witness loan rejection, from the lender's perspective they are high-risk applicants.

Therefore, businesses or applicants with “No Credit” or not much familiar with the banking should first start using the basic lending products like credit cards to maintain proper financial records and build a strong repayment capability. Also, ensure your usage towards credit utilization is not more than 30% of the actual sanctioned limit.

There are few industries that are known to be high riskier to invest in and always have high chances as far as failure is concerned. For instance, if a businessman wants to start a stock broking company, the entire work cycle of the company will be dependent on the market fluctuation.

Also, in past years the Covid pandemic has drastically changed the working system and livelihoods of many businesses. In such a scenario; It is not possible for banks or NBFCs to offer financial assistance to start a Gym, restaurant, cinema, travel company, shopping, hotel, mall..etc. The reason behind it is simple economical or environmental situations do not allow them to start or open these businesses as the high-risk ventures are considered by the lender.

Hence, the lending institution doesn’t want to provide small business loans to such industry-based companies.

Apart from the nature of the industry, there may be other external factors that may cause the rejection of a business loan application. For example, if there are any changes in the tax regulations by Government policies or Global factors that shall affect the lending institution decision-making process of the sector for a while.

Therefore, you need to be aware of other external factors that are impacting your business and submit your loan application smartly. You must avoid filing an application in such critical times such as recession, war, or any other geopolitical challenge in the economy that takes place.

Lending institutions prefer to fund those businesses that have at least a few years of experience and maintain a good track record. In case your business is newly established, you may face difficulties in availing of a business loan. These policies vary from lender to lender.

Without maintaining an effective financial record, your business loan application may get rejected because of the lender policies. Even if you have a good business and solid finances, the lender may require a business to be of minimum 3 years old before they could extend a loan.

Ideally, you should spend some more years in business before approaching loan facilities. Meanwhile, during the period would help you build a sustained cash flow along with a credit profile that may help in getting approval for a business loan.

However, there are still some lenders who offer credit facilities to new businesses with simplified criteria. To avoid loan rejection, you have to find the right lender who is willing to fund you.

One of the crucial reasons behind the small business loan rejection, most of the small businesses have small loan requirements as they do not have a too high need for cash at the initial phase of development.

Small businesses are easily manageable with lower funding. From the lender's point of view, the lower loan amount will not be profitable earning as the expected return is lower. This is the reason why lenders prefer funding for big-ticket projects/businesses as it is more profitable for them.

Hence, the borrowers need to assess and evaluate all the required aspects of the business and put the projection according to which they can apply for the loan.

Applicants’ legal/criminal history is given equivalent weightage to business history while considering a loan application. In case any of the founders, directors or key personnel in the business has a criminal history, it can be one of the reasons why your business loan application may get rejected.

Business funding is easily accessible to those who have a clean history and are not named in any illegal activities.

In case there is a minor criminal history the best you can do is disclose and explain the scenario in which the case was filed and how you come out from it. But if the offences seem serious, the lender strictly avoids processing your application.

Still, there is a chance of approval if you remove that specific founder or director from the company before submitting a loan application.

Now that you are aware of the reasons behind the loan rejection. The following are some of the tips that improve the chances of loan approval as follows below:

Improve your Credit Score: Your credit score is one of the most important measures of your financial health. It gives a clear idea about your repayment capability. Your past financial track record helps the lender to calculate the risk associated with your profile.

Therefore, maintaining a timely repayment cycle for business credit card bills, account receivables and other debt will boost your loan approval chances. The better your score is, the easier you will find it to be approved for new loans.

Pay off outstanding debts: On checking your credit history, lenders are keen to know if there are any running or outstanding debts on your profile. Paying off other outstanding loans would not only help in improving your debt-to-income ratio but also increase your borrowing capabilities.

Improve your tax Strategy: Have you ever thought that improving your tax strategy would help you in reducing the tax burden and increase your income. Hiring a professional to plan tax wisely will increase the chances of loan approval as the lender considers your tax return income as a measure of profitability.

Also Read: Tax Benefits on Business Loan in India

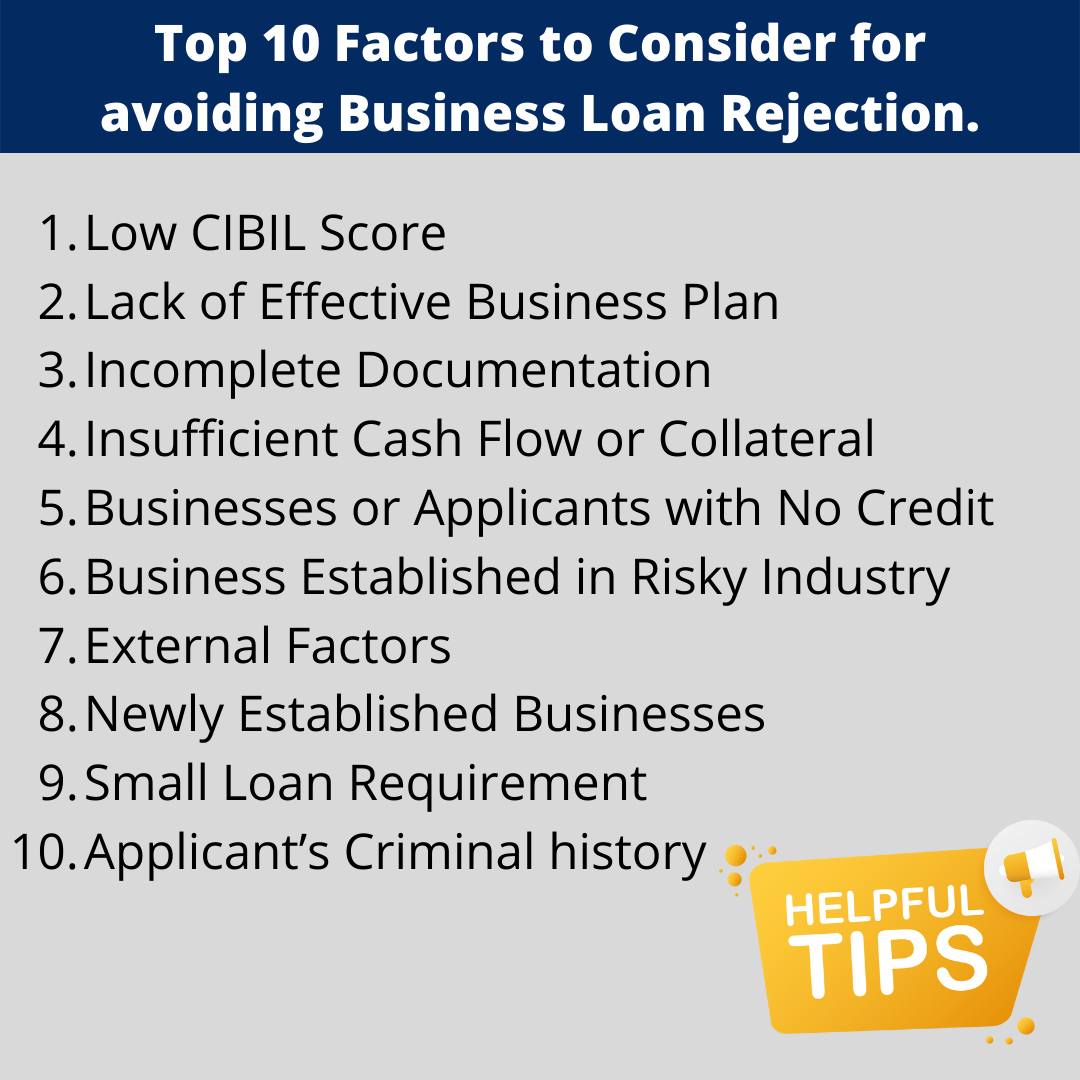

Above are the top 10 reasons why Indian businesses face rejection for small business loans. You need to keep these points in mind while applying for a small business loan.

You can also expand your existing business unit by getting a simplified business loan. Based on your requirements, you can take a customized business loan for a specific amount and flexible tenure that is suitable for your needs.

Financeseva.com is India’s leading online platform providing credit solutions for all personal and business needs under one umbrella from leading banks and NBFCs at competitive rates.

With Financeseva, you can easily compare and choose the best deal that matches your requirements and get a high-value sanction with a flexible repayment facility. The best part is that they work on your behalf starting from application to disbursement and provide end-to-end doorstep service.

CA Vikas Jain - Our Mentor