Your CIBIL score is a significant factor in analyzing whether you will be eligible for a loan or not.

A CIBIL score is generated on the basis of your credit history that includes total levels of debt of an individual, repayment history, length of credit history, type of loan, number of open accounts, etc.

CIBIL score is also known as credit score which is a three-digit number that generally ranges between 300 to 900. It is intended to show the credit risk.

A high score that is closer to 900 indicates strong creditworthiness and the chances of approval for the loan are higher while on the other hand a low credit score that ranges between 300 to 549 represents low creditworthiness and the chances to avail a loan are very less.

| CIBIL Score range | Status of credit health |

| 300 to 549 |

|

| 550 to 649 |

|

| 650 to 749 |

|

| 750 to 900 |

|

A good credit score provides you to get numerous benefits over those having lower credit scores. You are enabled to the following benefits if you have a good credit score.

If you have an excellent credit score, then there is less risk. And chances of approval for loans are higher.

One of the major advantages of having a good credit score is that the lenders may offer you loans at a lower rate of interest. You can also avail other benefits on processing fees and eligibility to avail of the higher loan amount.

An applicant with the excellent credit score is eligible to get pre-approved loan offers. Basically, pre-approved loan offers are provided to the existing borrowers who have a good credit history.

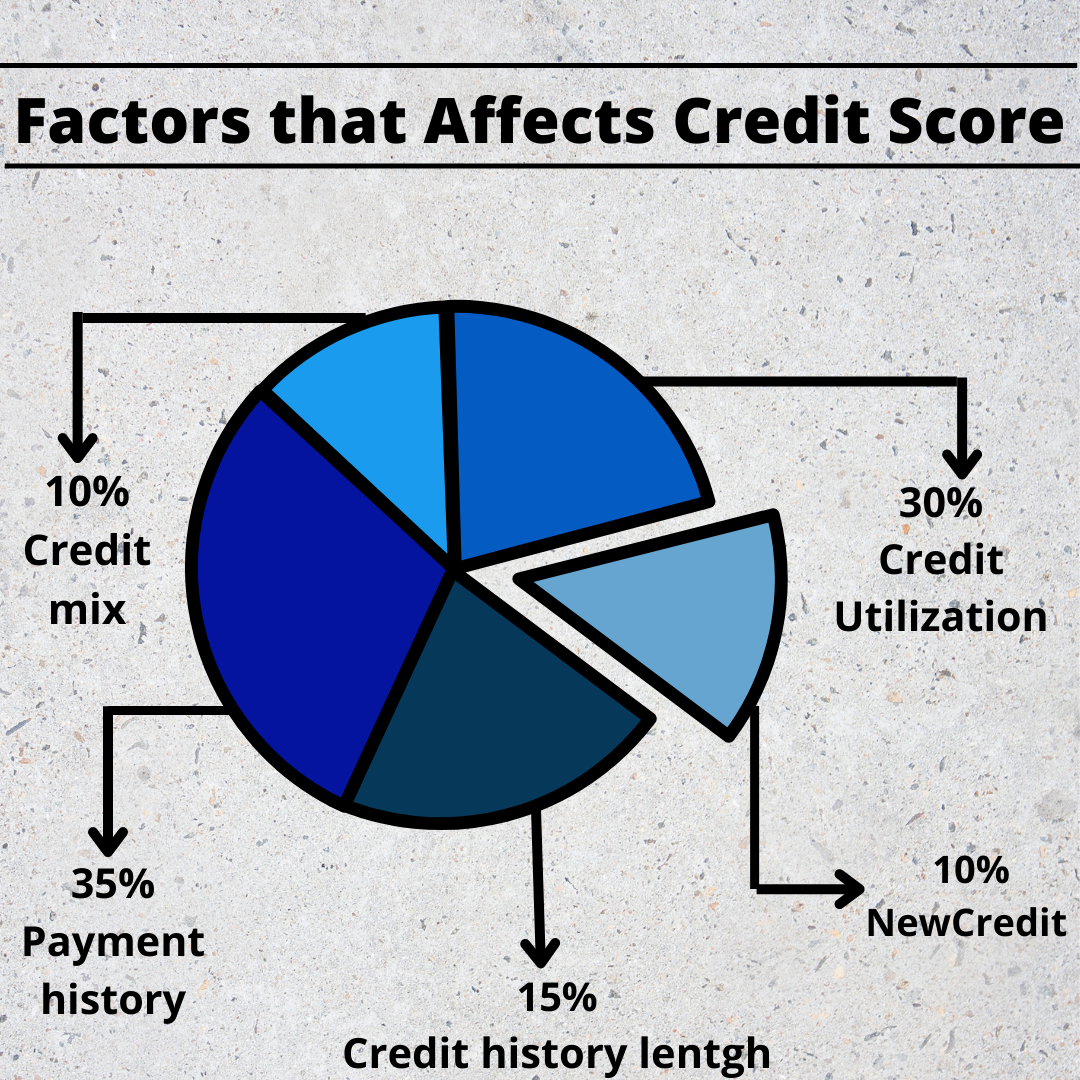

To calculate a credit score there are numerous factors that contain your payment history, application for credit, length of repayment history, credit mix, debt amount, etc.

Repayment history – Defaulting or overdue payments on your monthly installments will have a negative effect on your CIBIL Score. It is one of the most significant factors to consider in deciding your score.

Multiple inquiries – If you have many queries then you seem to be credit hunger. Banks are cautious about approving loan applications for such borrowers.

Credit utilization – Excess usage of credit shows that the borrower is extremely reliant on credit. Moreover, such behaviour cause to the rejection of a loan. Banks required a credit usage ratio of less than 30%.

A total number of loans applied for & are approved – The credit bureau will have all the records of loans applied in the past and the number of approved loans. If your record shows a lot of existing loans, then it might hurt your CIBIL Score.

As we all know, CIBIL Score plays an important role in availing a loan. Listed below are some factors to increase your score.

Check your credit score frequently as it stated a few things that are essential for your credit score such as information recorded in the credit report and the credit card or a loan where the delayed payment or defaults exists that lowers your CIBIL Score.

This assists you in fixing your score because if you track your score regularly to see if there are any delays or defaults in the payments.

Do not utilize your credit card for all the transactions as your credit utilization shows the ratio that you use on a given credit limit.

Make sure that you keep the credit utilization ratio at 30% or less.

Therefore, it allows you to pay lower repayment & makes your profile high creditworthiness.

When it comes to monthly installments, make sure that you pay the whole amount instead of paying the minimum amount due on your EMIs.

Repay the borrowed amount as soon as possible. And if you are unsure then go for a longer repayment schedule, hence it makes your monthly EMIs easy and low to pay it back without any hassle.

Avoid accessing loan applications from various lenders at the same time as it affects your CIBIL Score. And brings down the chances of availing a loan.

A credit score is an important document that the lender check, whether the borrower has applied for a loan.

It provides them with the idea that if borrowers can pay back the borrowed amount on time or not.

Moreover, it is important to have a good credit score and it can be maintained by checking credit reports regularly, making all the payments on time, keeping credit utilization below 30 percent, and paying off all the existing debt.

Not every person can access your credit report, some individuals, and institutions who are legally authorized can have access to it. If an organization has certain business requirements with you, it is safe to accept that they have access to your credit score and credit reports.

Listed below are some of the individuals and institutions that can access your credit report.

Banks – Banks can get access to your credit report to determine your creditworthiness. You do not need to have a credit card for lenders to have access.

Your creditworthiness may be reviewed if you are getting a loan or availing an overdraft facility.

Government agencies – If you are applying to conduct business with the government, court order, government benefits, etc... Then the government might make a report to figure out your financial standing.

Creditors – Anyone who is inclined to lend you money will have to decide your creditworthiness before putting their trust in you.

Evaluating your creditworthiness helps the creditors to assess whether you are capable of paying back the loan or not and helps the creditors to check the terms & conditions for the same.

Basically, the better your score is, the more you are likely to avail the approval of the loan and get an affordable rate of interest and flexible repayment tenure.

Insurance companies – It shows that the applicant with a poor credit score has to file a claim. These companies usually evaluate your creditworthiness to check how they require to charge for a new policy.

Employers – Many employers use credit reports to review honesty and sincerity when it comes to finance.

It can also be utilized to assess the risk to pay off, an individual with a lot of debt is affected financially and these reduces the concentration of work which might led to zero output.

Based on the financial activities, promotion and demotion are decided by the employees.

There are several reasons for a low CIBIL score. The score of the individual might reduce because of their dues and errors made by lenders.

Basically, mistakes made by lenders involve the failure of updated records and inaccurate information sent about an individual to CIBIL.

The essential factor that affects the credit score of an individual is their own behaviour.

Some applicants do not pay their bills of total EMI installments every month which leaves an outstanding balance on the loan. Hence, it lowers their score.

If the applicant utilized more than 30% of their credit limit, then it has highly affected their credit score & also shows their dependence on credit is high.

If an applicant is delayed in making the payments of EMI, then it will be shown on their credit report and therefore, it will reduce your CIBIL Score.

If an applicant applies for various loans then lenders verify their credit report or Cibil score for processing the credit card application and providing a loan. And if there are too many queries then it may result in a reduction of the score.

Listed below are several factors when determining a credit score -

Length of credit history – The time span of credit history is the time which is provided to the borrowers by the banks to pay back the borrowed amount of a product that the borrower has availed from the banks.

Type of credits – There are three forms of credit such as installment credit, revolving credit, and open credit. Credit enables people to purchase goods & services with borrowed money.

Payment history – The borrower should make Equated Monthly Installments (EMIs) and payments of monthly credit card bills. Payment delay may lead to a bad payment history and has a direct impact on CIBIL Score.

Credit mix – It also affects the CIBIL Score in comparison to the portfolio of the loan. The portfolio consists of unsecured credit lines against your name & number of secured loans.

Errors in a credit report – These are the common circumstances like wrong personal information which has a bad effect on the credit score.

What are the ranges of CIBIL Score?

The credit score ranges from 300 to 900.

What is a credit score?

The information elaborated on your credit report includes many variables that CIBIL uses to determine your credit score.

What are the information required to get a CIBIL score?

The personal information that is required to decide the score are PAN Card, E-mail address, Residential address, authentication, etc.

What is the minimum credit score to avail a loan?

The minimum score to get a loan range between 700 or above.

Who will use my CIBIL Score?

What is a good credit score?

A good credit score is considered to be 750 or above. If the score is within such range, then you can apply for loans.

What is a credit rating?

A credit rating is the other name of a credit score which is usually a digit number that ranges from 300 to 900.

Hence, knowing the facts about Credit score financeseva allows you to choose the best deals.

Also read: - Top 5 Benefits of Having a Credit Score Above 750

CA Vikas Jain - Our Mentor