A home loan is a big decision for individuals as it’s a long-term commitment in which you will be paying regular EMIs over a set of periods of time. Generally, the repayment tenure can be up to 30 years.

Most of you might have questions like is it necessary to continue with the same lender then the answer is obviously no, with a balance transfer facility; it is flexible to transfer your existing loan to another lender if they are offering a lower interest rate, better terms, other benefits or providing good customer service.

Table of Content

|

A home loan balance transfer is also known as shifting your outstanding home loan to a different lender for a better rate of interest. If you meet the required home loan eligibility, you can switch over and get a better deal on your balance transfer.

Typically, when you transfer your home loan to another lender, the new lender will pay off the unpaid balance loan amount on your behalf to your existing lender, by doing so your existing home loan account gets closed. Meanwhile, your new housing loan account begins with the new lender, where you will be paying a lower home loan interest rate.

Many banks and housing finance companies offer home loan balance transfer facilities. If the new bank’s interest rate plus these additional charges still prove to be cheaper than the current loan, only then should a customer choose to refinance the loan. The process of balance transferring the housing loan will encourage many homeowners.

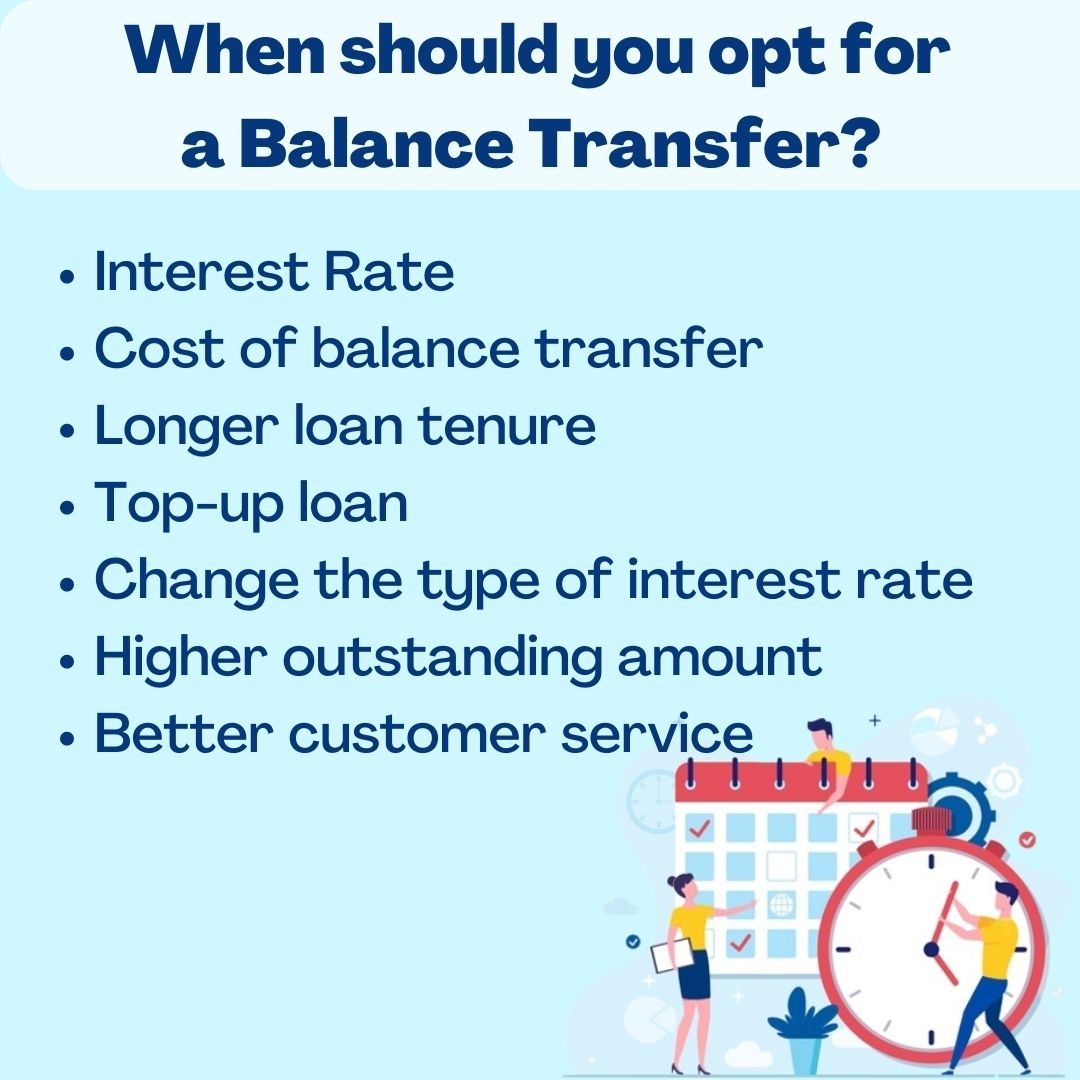

However, the decision should be typically based on one’s financial conditions by the transfer to the consumers with excellent credit scores. In most cases, borrowers are confused to estimate what is the right time to balance transfer the home loan. Let’s examine the aspects in detail.

The general perspective of most borrowers is if another lender is offering a better interest rate, then he/she must transfer it immediately. The natural will be tempted to go for a new lender which consequently brings down your EMI by reducing the interest rate as the existing loan is being transferred to a new lender.

Most often borrowers get attracted when it comes to an affordable and quick solution as compared to other lending solutions. However, factors to be taken care of before you transfer your home loan balance. Borrowers must do in-depth research and cost analysis of the benefits by figuring out the values.

The lowest rate of interest is the most common reason for transferring a home loan. Even a tiny difference of 1.00% p.a. in the interest rate makes a difference in the overall amount paid.

In the table below, given a difference between without balance transfer and with a balance transfer to demonstrate the benefit of the lower rate.

| Category | Without Balance Transfer | With Balance Transfer |

| Loan Amount | 50,00,000 | 50,00,000 |

| Loan Tenure | 20 Years | 20 Years |

| Interest Rate | 8.00% | 7.00% |

| Interest to be paid | 50,37,281 | 43,03,587 |

| Monthly EMIs | 41822 | 38765 |

Now it is clear from the above table that the change of 1.00% in the interest rate resulted in a great difference of Rs. 73,3694 in the interest rate paid.

Most individuals assume that interest rate is the only cost that needs to be considered while transferring a home loan balance. But in reality, it is not like that, there are several costs involved that need to be given equivalent consideration while making a long-term commitment to a home loan balance transfer.

So, it’s always better to read all the guidelines and fine print before approaching a new lender. Do not avoid or ignore any hidden charges prior you make any decision.

The benefits you get should be more than the cost involved in the processing fee or other charges. Evaluate that the additional cost is still less than your interest amount to ensure the transfer is worth paying all the charges.

If the balance transfer is not having an efficient result, then borrowers may also consider the option of resetting the loan.

The maximum tenure of a home loan helps you to save the maximum amount with a reduced interest rate. Home loan tenure can be up to 30 years. It proves to be beneficial if you are using the transfer facility at the initial stage of repayment. Since, taking a balance transfer when you are almost near to end up loan tenure does not make any sense.

Lenders consider that when you still have a longer loan tenure left in such cases, one can switch the lender to enjoy better lower rates and other benefits. You should steer away from such home loan teaser schemes, because when rates are increased, it potentially outdoes the benefit of a lower rates enjoyed for a couple of years, making it worthless. You can also reduce your EMI by choosing a shorter tenure and making it more convenient to repay the loan easier and quicker.

A top-up loan is a facility that can be sanctioned with a balance transfer and be taken over the home loan. While transferring the loan, the borrower can get an additional amount from their existing loan.

The additional amount is called a top-up loan facility and is availed at competitive interest rates. It gives a greater level of flexibility on which you can use these funds for any personal purposes be it wedding expenses, financing children's higher education, renovating homes, and much more.

A borrower should only go for the additional loan if required and if they get the benefit of lower rates. Make sure that you get a good rate of interest when you are applying for a top-up loan on a home loan balance transfer.

For example, let’s take Mr. Arvind who had taken a home loan of Rs.50 lakh for Rs.95 lakh property value (five years ago). After paying EMIs for 10 years. Let’s assume that for 10 years the loan balance comes down to Rs.30 lakh and in the meanwhile, the property value has risen to 1.25 Crore.

In such a scenario, Mr. Arvind can get his loan transferred to another lender along with the outstanding of Rs.30 lakh loan amount at a lower interest, and also get additional funding of Rs. 20 lakh more or less at the same home loan interest rate. They have the flexibility to borrow additional loans generally limited to 25% of the outstanding amount from the bank at the prevailing rates.

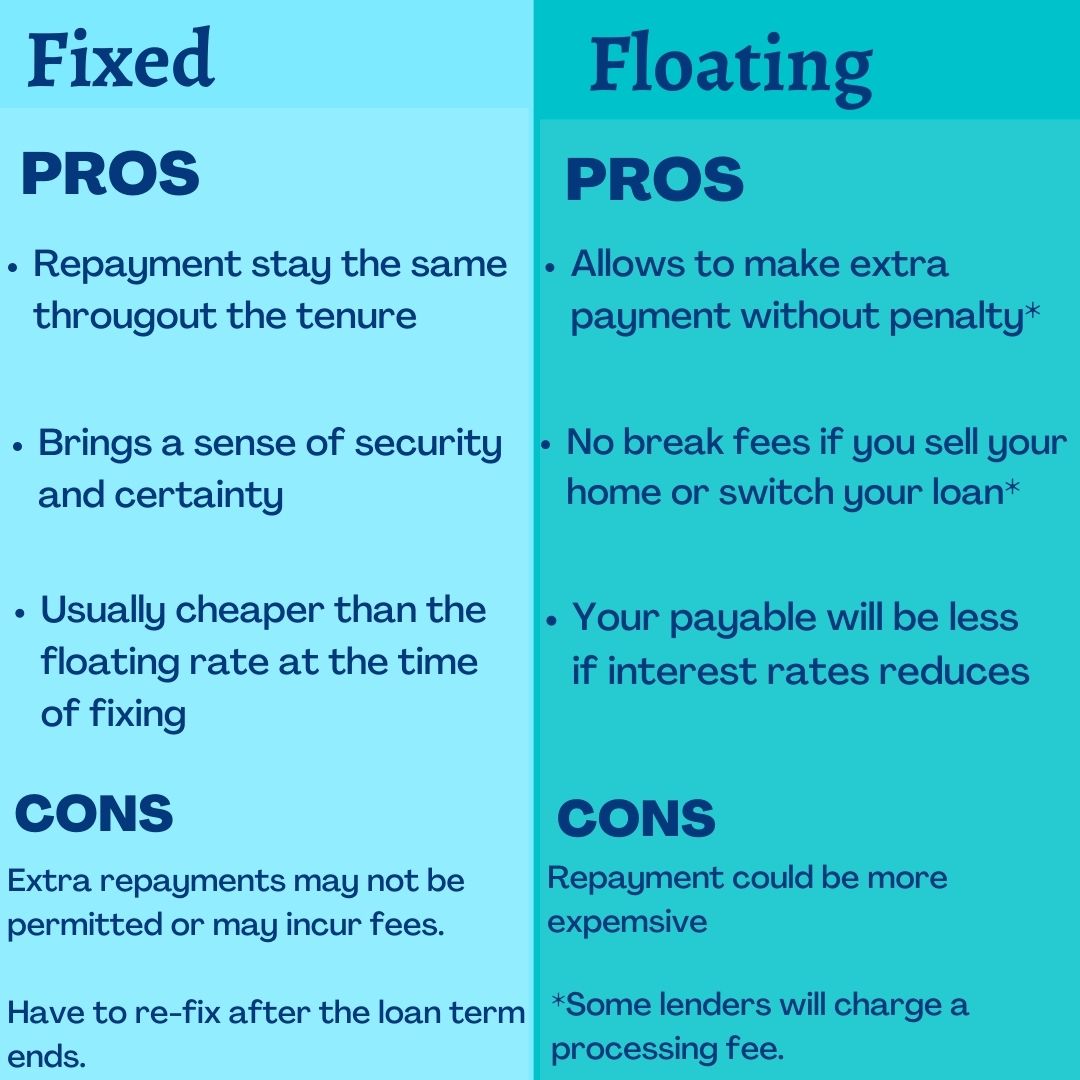

A housing loan can be availed as a fixed or floating interest rate. A fixed interest rate will remain the same throughout the loan tenure.

Whereas floating interest rate changes are based on repo rate changes. With a home loan balance transfer, one can change the type of interest rate he or she is paying.

This is important because in your initial years you pay most of your principal amount. A floating interest rate on a home loan implies that the lending rate will be subject to revision every quarterly. With changes in the base rate, the interest rate changed on your loan will also vary.

Get Low Rates on Balance Transfer

If you are paying a floating interest rate on your housing loan and you see that home loan interest rates are increasing continuously, then it is recommended to switch to a fixed rate. While on the other hand, let us consider you are paying a fixed rate and see a possibility of reducing and at that time, switching to a floating rate will prove to be beneficial.

While switching from a fixed interest rate to a floating interest rate and vice versa, a balance transfer should be considered to get the benefit of a lower rate of interest.

In case you are not happy with the current lender, the option of a balance transfer is always open for you to take a switchover.

Also Read: Know everything about low interest rates for home loans

While transferring housing loans, make sure that the outstanding balance amount is higher. It is advisable to switch your loan when a higher portion of your debt is unpaid. Otherwise, avoid when there is only a small amount is outstanding.

Let’s take if there is a higher outstanding amount, then the balance transfer will aid you in reducing the interest paid amount and turn out to be profitable. However, in the case of a lower outstanding amount, the balance transfer will not result in profitable because of the cost involvement such as the charge and processing fee to the new lender. Ensure that the outstanding amount and the money you will save from transferring the loan are worth enough to save your time and efforts.

The housing loan repayment duration is usually longer as compared to other loans. Since, this is a long-term commitment so most borrowers is keen on good customer service. There can be several issues you may face after taking a loan, such as no proper service, not updating details even after a long conversation, implementing frequent changes on terms and conditions.

However, shift to a different lender. If your existing isn’t offering such services you can transfer your outstanding housing loan. So, you can switch to another lender with whom you are comfortable.

The following are the process for home loan balance transfer:

Step 1 - Compare offers for a balance transfer with other lenders and compare their interest rates along with their benefits, processing, and other charges.

Step 2 - Once you get a better deal, negotiate the terms with your current lender to see if they can offer you the same or better loan terms.

Step 3 - Once you decide to go ahead with the transfer, get a NOC (No Objection Certificate), loan repayment record, and property documents from your existing lender.

Step 4 - Make sure that you take away the property documents from the existing lender or they would directly transfer them with the new lender. Your existing lender will issue a NOC (No Objection Certificate) along with the remaining loan transfer.

Step 5- In the meanwhile, start the home loan application process with the new lender by submitting the application form and all other required documents.

Step 6- Get a sanction letter and sign the loan agreement whether the bank has included a penal charges clause for a balance transfer with the new lender.

Step 7- Once the previous lender receives the outstanding loan amount, they will cancel all the cheques and ECS (Electronic Clearing Service) and close your home loan account.

The bank leverages a transfer cost on doing such a balance transfer. In some cases, you might be charged by both the existing and new lender. There are several costs associated with your balance transfer, including processing fees, technical fees, legal and valuation fees. Usually, stamp duty would cost around 0.20% to 0.50% depending on the location and, processing charges 0.50% to 1% fee. So, it’s always better to read all the rules and fine print before avoiding any hidden charges and then make an informed decision accordingly.

You have to pay a balance transfer fee, though fees will typically cost you less than you should be paying in interest. If the new lender is offering an affordable rate of interest with other additional charges that still seem to be lower than the current loan paying, then choose a refinance loan.

The transferring of your housing loan involves several charges. The interest rate on your housing loan may reduce after refinancing a home loan. Opting for a BT at the starting loan tenure will not be beneficial, because you will have a processing fee and other charges, moving to a new one can affect your saving. Consider all these costs when refinancing and cross-examine whether the additional costs are still less than your actual interest rate. Evaluate if the transfer is worth paying all the charges.

Since it requires you to pay the repayment in the same monthly installments year on year, until the end of the loan tenure. Fixed-rate interest means that the rate doesn’t change with the market and borrowers are given the option to look at the interest rate as per their ideal budget.

Therefore, if you would like to cut interest costs when taking the loan, then you should opt for a floating interest rate. In the case of floating home loans, the rates are adjustable as per the market fluctuations.

For example, let’s assume that the floating interest rate is 10.50% and the fixed rate of interest is 12% which ends up saving a lot of money when there is a difference in interest rate by 1.50%. The floating interest rate can be changed to a fixed rate but does not apply throughout the loan tenure.

However, the floating rate of interest is not a good option for those individuals who prefer to plan their budget in advance since the rates are changed frequently. But, these types of interest rates make it hard for one to plan his/her financials for long periods.

As a borrower, you need to think of the lowest interest rate and the prospect of a great lender and also consider other equally major elements.

The interest rate applicable in your case will depend on several factors such as type of property, income profile, and credit history among others. Depending upon the existing market position, try to negotiate for the lowest interest rate. However, the entire process would become easier and even smoother if you have a good relationship with the new lender.

Check with your new lender about the interest rate credentials. For example, let’s take if the new lender is advertising a lower interest rate, then you must ask them for more information on their interest record. Make sure the advertised interest rate is real or for sake of an attention-grabbing.

Leveraging a good credit/CIBIL score will help you in saving money and make your financial life much more affordable. If you have a good credit score, you can bargain for the best possible borrowing terms. A borrower with a solid credit profile and a CIBIL score of more than 750 will give you the choice to pick from the best lenders.

A good credit score is a key parameter considered by the lender and this can be possible if you have an error-free credit history. Based on your existing credit history, the lender determines your repayment capacity.

Check your Credit Score for FREE

Another important factor to consider before opting for a balance transfer, do a detailed study of the new lender’s terms and conditions before making a commitment. Avoid troubling yourself from entering into a long-term contract that might affect your finances. Be familiar with the terms of the new lender. This will help you in avoiding unexpected suspense such as hidden charges.

Thereby, it is recommended that you do due diligence yourself before making a decision ahead with your new lender for balance transfers.

If you’re almost near to end of your loan tenure, then applying for a home loan balance transfer doesn’t make any sense. If you want additional funds then you may opt for a top-up loan, which enhances your loan tenure.

Make a wise choice in selecting the type of facility you need based on your actual requirements.

For example, suppose you have a home loan of 70 lakh rupees for 25 years and you repaid it for 10 years and you plan for a home loan transfer to another institution, you can keep the loan tenure of 15 years, or you can go for a 25-year fresh tenure.

Also, in both cases if your home loan interest is lower by 0.5% you will have to pay a lower EMI. Total interest outflow will lead by 4 lakhs if u take the new loan for 15 years with the new lender, after repaying the loan for 10 years with the old lender.

Also Read: Things you must know before transferring your home loan

A home loan balance transfer is the common type of loan transfer, and it is generally used to lower interest rates on the running home loan.

For example, let’s assume by taking you are an existing borrower & decide to transfer your ABC bank home loan after 7 years to XYZ bank on a lower rate and changed tenure, depending on the current repayment range, you are basically opting for a balance transfer facility.

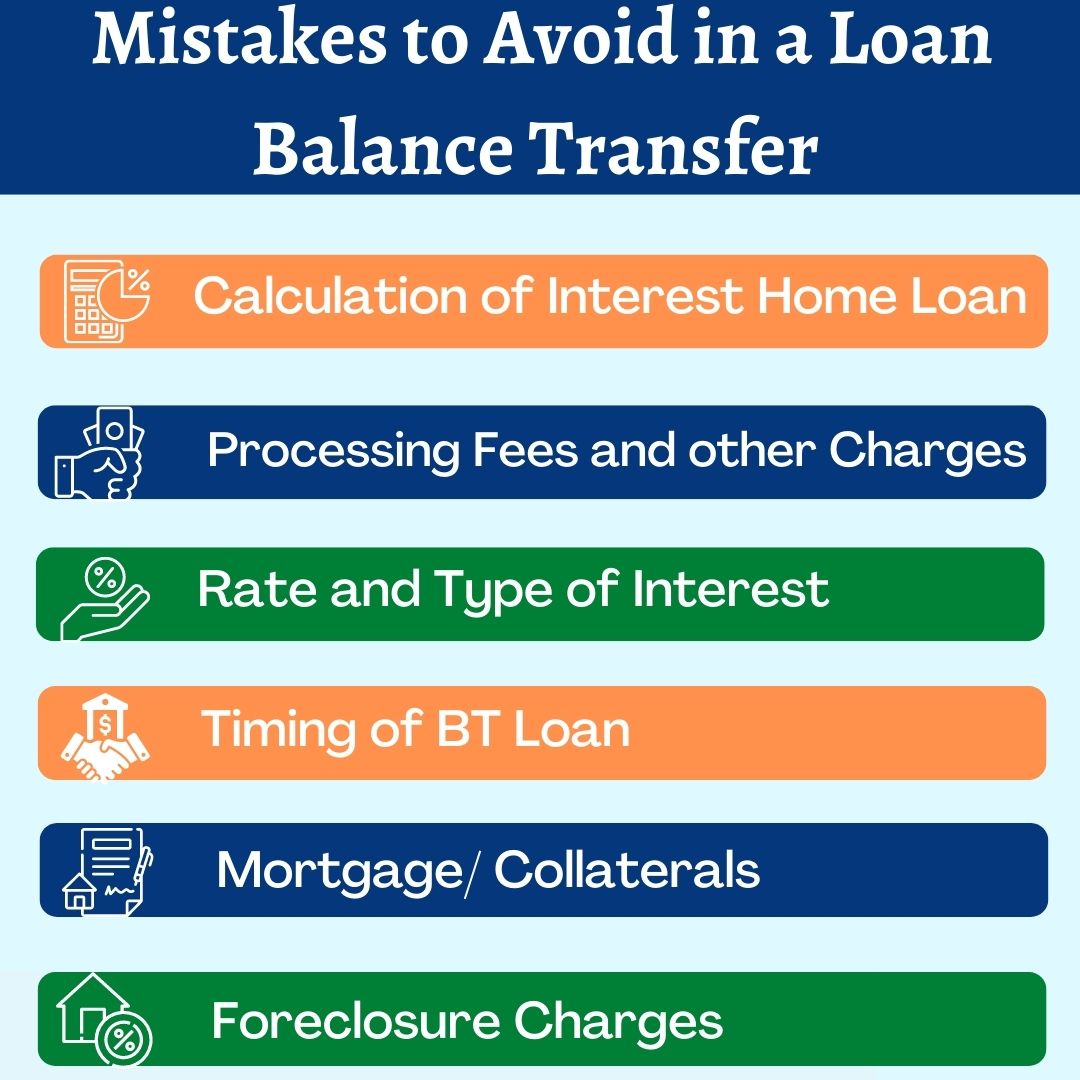

However, like with any financial decision, you’re making mistakes even during a balance transfer. Lossing more money in a wipe to home loan interest rate. There are several types of mistakes to avoid in a loan balance transfer:

Many times, borrowers who opt for a home loan balance transfer for a lower rate of interest but end up with a longer tenure. Do not transfer your loan amount without making an effective calculation of the total effect on your loan transfer.

Lower interest rates may be eye-catching and seem to be pocket friendly, however as you extend the loan tenure, the total interest paid on your loan will also increase so it is important to calculate the amount repaid before taking a decision. To get smaller EMIs, you might opt for a longer tenure. but this could only increase the debt burden. With longer tenure, you will end up paying more interest.

There are several expenses associated with balance transfer like the BT fee, the expense of stamp paper, processing charges, and other linked charges. So, always consider these charges before making a decision.

Sometimes, the loan transfer charges may depend on the type of income a person has; for example, a salaried person may be charged differently while a businessman might have a different charge.

In some cases, the charges of loan transfer vary depending on the type of income an individual earns; For example, a salaried individual may be charged differently as compared to a businessman.

So, make sure to ask the prospective lender about everything, they will help you know the charges before making a commitment.

The rate of interest is the most common factor to consider when applying for a home loan balance transfer. Therefore, make sure you compare interest rates and be aware of the type of interest rate.

Fixed interest costs you more than higher as compared to reducing interest rates. However, fixed rates frequently change depending upon the market fluctuation. Do not forget to go through an in-depth study about the type and rate of interest your lender is offering you.

Most borrowers make a common mistake of transferring the existing loan in which they might left over a few months of tenure to end up. Transferring loans at the end will increase the burden of the loan.

To avail of the maximum benefits, you should transfer the loan within the first half of the loan tenure. Such a loan transfer will not be a burden on the consumer. If a person has already crossed half of his loan period then it is better to wait till the loan maturity or take a fresh loan.

To avail of maximum benefits and reduce the loan burden you should transfer the loan in the initial time of loan tenure. By doing so, you will help you save on interest costs. If you have already crossed half of the loan tenure, it is better to wait until the loan maturity or take a fresh loan.

Almost every bank and financial institution ask for your assets to be guaranteed for a secure loan repayment because banks want to minimize the risk of repayment of the loan before granting the credit facility.

Transferring a loan without making proper calculations may lead to excessive payment and an increase in the loan burden. So, never make the mistake of pledging higher value collateral than the required loan amount.

However, financial decisions should not be taken in a hurried manner. Things involving huge amounts of money are often sensitive and should be followed with the utmost care. Generally, with a home loan balance transfer the banks provide a maximum loan amount of up to 85% of the loan against the value of a property.

Suppose you want a home loan for buying a property of Rs. 50 lakhs, the maximum amount you can get is 85% which means 42.50 lakhs. You can reduce your EMIs by switching to a lower interest rate offering lender. In addition, you can also get a top-up loan facility up to Rs.50 lakh with a host of benefits such as NIL foreclosure charges and zero pre-payment.

6. Foreclosure Charges

If you get additional funds in the future, you may want to foreclose your home loan in-between the loan tenure. Therefore, it’s important to check whether the prospective lender is charging for foreclosure before proceeding to transfer the loan to a different lender.

If the lender charges heavy foreclosure fees, it may further add to the cost of the loan.

Also Read: Top 10 factors to consider while taking a home loan

When the home loan becomes difficult to repay due to high-interest rates, the outstanding principal amount can be transferred from the existing lender to a new lender on better terms. Balance transfer refers to transferring the financial institution's outstanding home loan balance from one lender to another in this process is called balance transfer refinancing. In addition, a top-up loan besides balance transfer eases financial complications. This is a home loan balance transfer top-up which can be calculated by using a balance transfer top-up calculator.

A home loan balance transfer is a great way to get the benefit of a lower rate of interest and other associated benefits as defined above. Might the reason behind availing of a balance transfer vary? However, it is recommended to check the terms and conditions of the new lender and compare all the financial benefits before applying for it.

Financeseva allows you to compare and check those details on a single platform also you can use the EMI calculator to pre-plan your budget wisely.

Q1. What is a home loan balance transfer?

Balance transfer allows borrowers to transfer their current loan obligations from one bank to another. Generally, borrowers opt for BT when they get better offers from a new lender in terms of interest rates and other benefits.

Q2. When should you consider a home loan balance transfer?

Opt for a balance transfer, when the outstanding loan amount is higher to get a maximum benefit. Therefore, it is recommended to transfer a home loan when the outstanding amount is higher. The decision is to be made based on the outstanding loan amount and when the opportunity seems to be a better deal from other lenders.

Q3. How much time will it take to transfer a home loan?

The entire process of a home loan takes around 15 to 20 days to switch lenders. Hence, you have to obtain a NOC (No objection certificate) and apply with the new lender. However, the new lender will assess your application and check your eligibility to make sure that you have enough creditworthiness.

Q4. How does a home loan balance transfer work?

Once you have carried out a cost-benefit analysis to conclude that a balance transfer would be a beneficial option, you need to obtain a NOC from a balance transfer with the new lender.

Q5. What is the maximum limit of a home loan balance transfer?

Let’s take you are making a home loan balance transfer from one bank to another bank. The maximum amount to be transferred is equal to the outstanding balance amount.

Q6. What are the benefits of a home loan balance transfer?

The primary benefit of opting for a balance transfer is to avail a lower interest rate and reduce your EMIs. In addition, you can also avail a considerable top-up loan at an attractive rate of interest.

CA Vikas Jain - Our Mentor