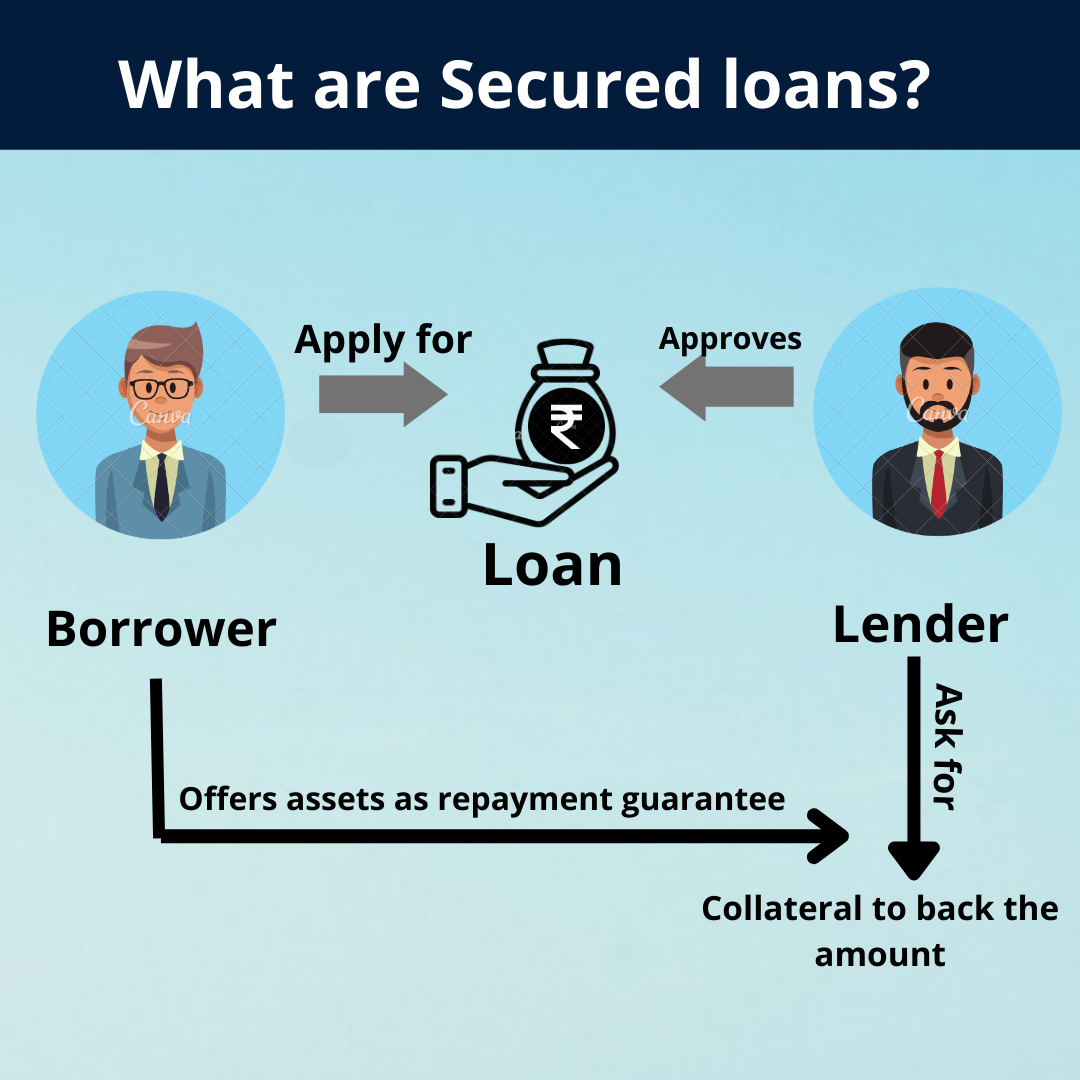

A secured loan is a form of debt where the borrower mortgages their immovable property to get the required funds.

The loan amount offered to the borrowers is based on the value of security or collateral.

There are several banks and financial bodies that will authorize the ownership deed of security till the borrowed amount is paid off.

The borrower can avail a lower rate of interest with a flexible repayment tenure because the borrower has given their property as security or collateral and the lender can have the benefit of the lower risk profile.

Listed below are the several types of secure loan: -

| Loan against property | Working capital loan | LC Discounting |

| Used Car loan | Letter of credit | Bank overdraft |

| Home loan | NRI home loan | Business loan |

| Loan against rent receivable | NRI loan against property | Commercial property loan |

| Infrastructure construction loan | Loan against bank guarantee | Building inventory funding |

| Used car loan | Drop line overdraft | Bank guarantee |

| Loan against securities | Home construction loan | Industrial property loan |

A loan against property is a secured loan that is offered by banks or financial institutions against freehold residential, constructed, or commercial properties. It is also called mortgage loan.

| Interest rate | @7.00% |

| Loan tenure | Up to 15 years |

| Loan amount | Up to 130% of property value |

| Processing fee | 1% to 2% of the loan amount |

A working capital loan is a loan that can be used to finance the daily operations of a business. It can be used to cover recurring expenses like wages, rent, accounts payable, etc.

| Interest rate | @6.00% |

| Loan amount | 200% of the property value |

| Processing fee | 0.5% to 2.00% |

A commercial property loan is the credit option that lenders provide against the mortgage of commercial property. These loans are of two types i.e., retail outlet and office space.

| Interest rate | @7.25% onwards per annum |

| Loan amount | From Rs. 5 lakhs to Rs. 5 crores |

| Repayment tenure | Up to 15 years |

| Processing fee | Up to 1% of the loan amount |

A loan provided by lenders keeping the future rent of the property as collateral. It can be taken by those applicants who own any kind of property.

| Interest rate | @8.75% onwards |

| Loan amount | Up to 85% of property value |

| Processing fee | 0.5% to 1% of the loan amount |

A bank overdraft loan is offered by the banks that allow the borrower to pay for bills and other expenses when the account balance reaches zero. The rate of interest of bank overdraft is @9.00% onwards with a flexible repayment tenure.

A home loan is a secured loan that can avail from banks, NBFCs, or financial institutions for the purpose of purchasing a residential property.

| Interest rate | @6.40% onwards |

| Loan amount | 90% of the property value |

| Processing fee | Up to 0.5% to 2% |

Home construction loan is a loan that is offered to individuals who own a piece of land and do not have the fund to construct their home.

| Rate of interest | @6.95% onwards |

| Loan amount | Up to Rs. 3.5 crores |

| Loan tenure | Longer tenure |

| Processing fee | @0.5% to 2.00% |

Secured loan provides opportunities to the borrowers to avail the required finance on better terms. It can be used for many different purposes such as bad credit loans, vehicle loans, mortgages loans, etc.

There are 2 factors from the banker's and borrower's points of view.

Pledged collateral can be used as loan coverage while on the other hand an unsecured loan carries a high risk of default.

| Bank name | Home loan | Used Car loan | LC Discounting |

| Axis bank | 6.70% | 14.80% | 8% |

| State Bank of India | 6.70% | 9.90% | 8% |

| Kotak Mahindra Bank | 6.65% | 11.20% | 5% |

| ICICI Bank | 6.70% | 10.20% | 5.50% |

| HDFC Bank | 6.65% | 13.75% | 8% |

Low interest rates: - Collateral loans are offered at a lower interest rate, as the borrower takes loan against collateral and the banks have trust in the repayment capacity of the borrowers.

High loan amount: - Banks provide large amount of loans, as the risk and liability are reduced.

Fast processing and approval: - The procedure of loan does not take much time, therefore there is quick approval of loan.

Flexible repayment tenure: - Under collateral loan, borrowers have a choice of repayment options that increase the flexibility of repayment.

Tax Deductible: - For home loans, the interest on the loan amount is tax deductible and saves money of the individual.

| Pros | Cons |

| The banks will provide a higher borrowing limit that permits to get a large amount of loan. | Floating interest rate can led to repayment tenure. |

| The borrower can pay the nominal rate or interest on the borrowed amount. | The possibility of losing collateral may occur if the applicant failed to pay the borrowed amount. |

| A loan can be offered for a longer repayment tenure. | A longer repayment schedule might result in a high interest payable over the tenure. |

Applicants can pledge various types of assets. Given below are some assets that are commonly used as collateral or security.

| Details | Secured loan | Unsecured loan |

| Loan amount | High | Low |

| Loan tenure | 15 to 30 years | Up to 5 years |

| Collateral | Required | Not required |

| Rate of interest | Low | High |

| documentation | More documents required | Less documentation |

| Speed of disbursement | Slow | Very fast |

| Examples | Home loan, loan against property, car loan, etc. | Education loan, personal loan, credit card purchase, etc. |

Step by step to apply online: -

Step 1: - Visit the official website of your preferred bank & verify your loan eligibility.

Step 2: - With the use of EMI calculator, you can calculate your monthly payable EMI.

Step 3: - After evaluating your EMI, start filling in the application form.

Step 4: - Enter all the required details and select the needed loan amount and loan tenure.

Step 5: - After filling in the application form, click on ‘Submit’.

Step 6: - Then, the bank representative will get in touch with you for further formalities after reviewing your application.

Step 1: - Visit the bank branch of preferred lender.

Step 2: - Ask for a secure loan application form and fill in all the required information.

Step 3: - Submit all the relevant documents such as age proof, income, address, identity, etc.

Step 4: - The bank representative will verify documents and check the eligibility of the borrower.

Step 5: - Then, the amount of the loan will be transferred to the bank account of the borrower.

Financeseva offers more than 80+ customized loan products for individuals and businesses. Applying with financeseva will help you to get the best loan offers at a single platform and easy approval.

Also read: - Difference Between Secured Loan vs Unsecured Loans

CA Vikas Jain - Our Mentor