If registration has been canceled under clause (b) or clause (c) of subsection (2) of section 29 (I.e. non filing of returns ) on or before the 31st day of December 2022, and the registered person has failed to apply for revocation of cancellation of such registration within the time period ( I.e. 30 days from date of service of cancellation order ) specified in section 30.

The CBIC has given one time opportunity to the registered person to revocation or cancellation of registration, by applying the following procedure.

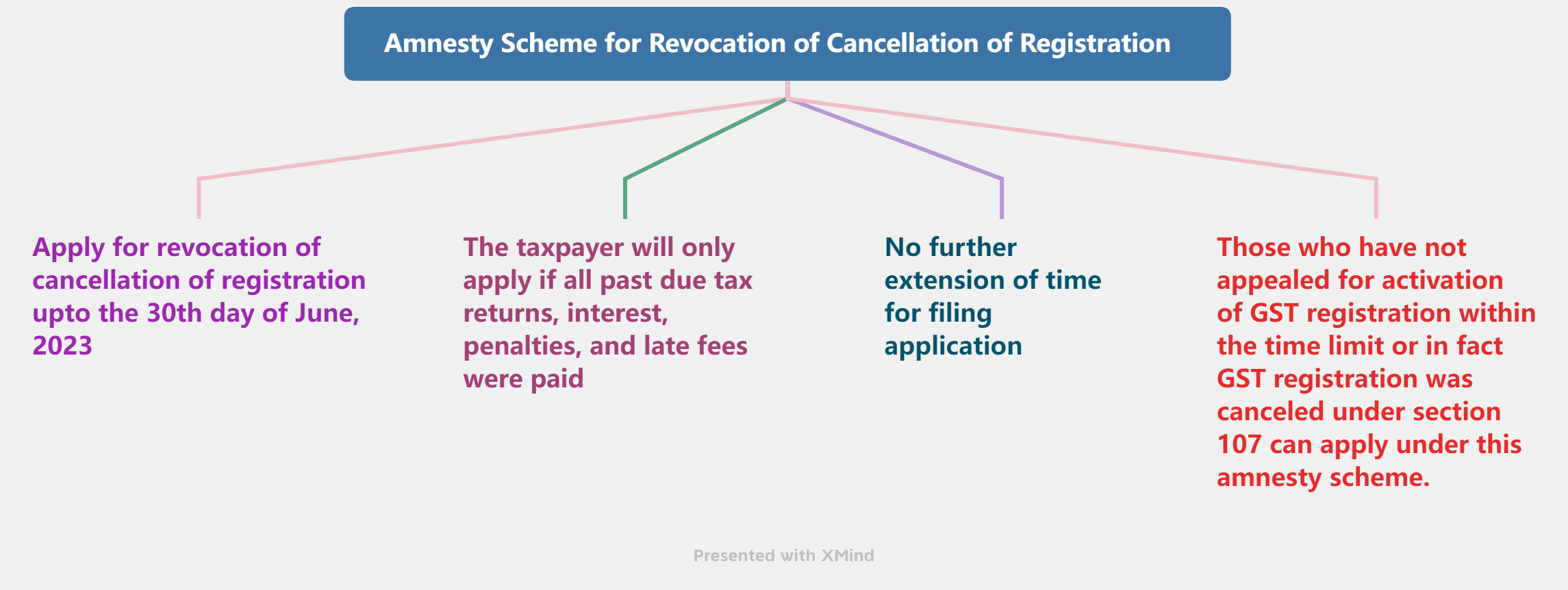

(a) the registered person may apply for revocation of cancellation of such registration upto the 30th day of June 2023;

(b) the application for revocation shall be filed only after furnishing the returns due up to the effective date of cancellation of registration and after payment of any amount due as tax, in terms of such returns, along with any amount payable towards interest, penalty, and late fee in respect of such returns;

(c) no further extension of time for filing an application for revocation of cancellation of registration shall be available in such cases.

The benefit of this amnesty is also available for the registered person

whose appeal against the order of cancellation of registration or the order rejecting the application for revocation of cancellation of registration under section 107 of the said Act has been rejected on the ground of failure to adhere to the time limit (30 days from date of service of cancellation order) specified under sub-section (1) of section 30 of the said Act.

CA Vikas Jain - Our Mentor