.png)

we mirror your general "What we Do" structure but specializing for MUDRA scheme.

The Pradhan Mantri Yojana (PMMY) enables micro-credit to non-farm, non-corporate

The following categories of applicants are eligible to apply for a MUDRA Loan:

Micro and small enterprises in manufacturing or service sectors

New entrepreneurs planning to start a business

Retailers, shop owners, and traders

Start-ups and self-employed individuals

Agriculture-allied activities such as dairy, poultry, fisheries, etc.

Small-scale units such as mobile repair, tailoring, beauty salons, motor garages, etc.

Transport operators and MSME business owners

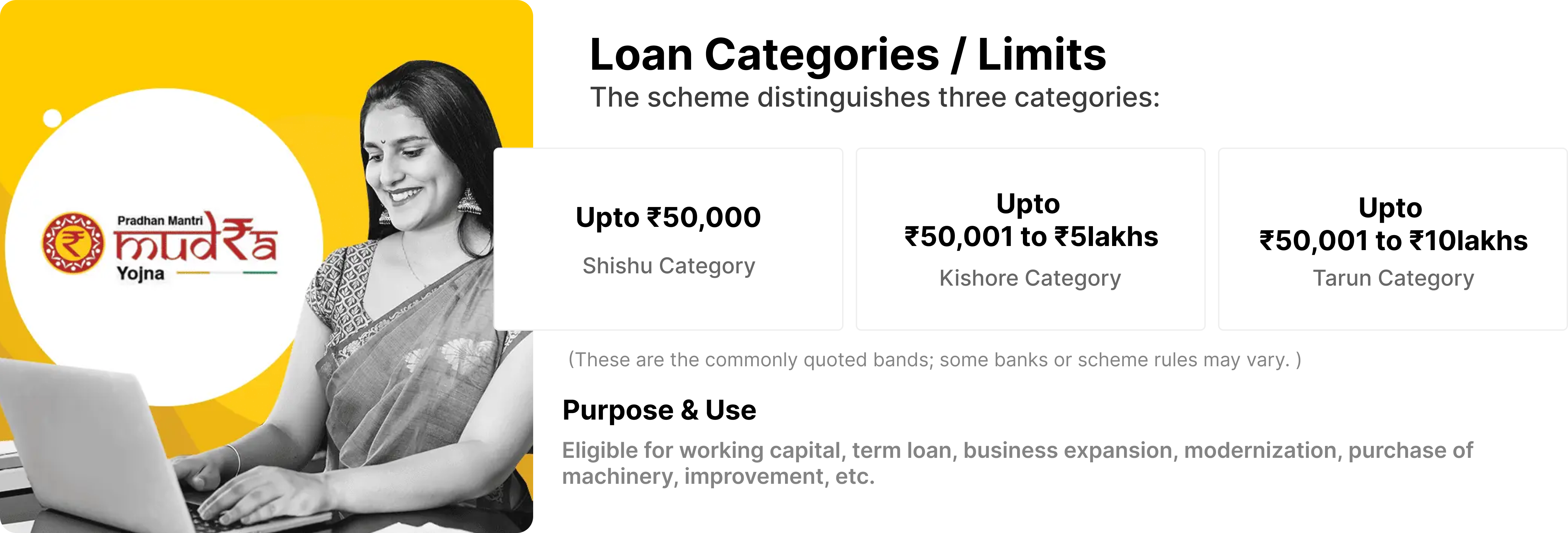

Loans are provided under three categories — Shishu, Kishor, and Tarun — based on the stage and scale of the business.

Under the MUDRA scheme, financial assistance is offered as follows:

Shishu: Up to ?50,000 (for new businesses and initial working requirements)

Kishor: ?50,000 to ?5 lakh (for growth and expansion of existing businesses)

Tarun: ?5 lakh to ?10 lakh (for well-established businesses aiming for higher scaling)

Collateral-free loans

Attractive interest rates (as per individual bank norms)

Flexible repayment options

Term Loan and Working Capital facilities available

Issuance of MUDRA Card by the bank, wherever required

MSME/Udyam Registration recommended for added benefits

Loans under PMMY are strictly for business purposes and not for personal use.

The scheme is implemented through all public sector banks, private banks, RRBs, NBFCs, and Micro Finance Institutions.

Common documents required include: Aadhaar, PAN, business plan, bank statements, and financial projections.

Women entrepreneurs may receive preferential benefits and lower interest rates depending on the bank.

Loan approval depends on business feasibility, bank discretion, and applicant’s credit profile (CIBIL).

Answer few questions and get matched with best suitable scheme(s).

Provide basic details & documents and the advanced technologies would capture/auto-fill required details through smart analytics.

View offers from 200+ Lenders and get Digital Approval from selected bank.

Check the real time status of your application at your convenience.

Up to ₹50,000 (Shishu): typically no margin required.

₹50,001 to ₹10 lakh: margin may apply (e.g., 20%) depending on lender policies.

Collateral or security may be required as per bank & scheme norms, unless covered under guarantee schemes.

For loans up to ₹5 lakh: maximum tenure around 5 years including moratorium of up to 6 months

For loans between ₹5 lakh to ₹10 lakh: maximum up to 7 years including moratorium period of up to 12 months

The scheme is supported by guarantee cover under a Central guarantee mechanism (e.g. via NCGTC / CGFMU) so that small borrowers can avail collateral-free credit to some extent.

Competitive interest rates as per bank norms + applicable taxes.

Processing / upfront fees: often nil for Shishu / Kishore in many banks; for Tarun could be ~0.50% (plus tax) (varies by bank).

Other scheme charges, guarantee fees, etc. may apply.

We provide weekly status updates and help close queries quickly.

For Shishu (up to ?50,000), often minimal documentation is needed. For Kishor (?50,001 – ?5,00,000) and Tarun (?5,00,001 – ?10,00,000) categories, a robust project report greatly increases approval chances.

Yes, we deliver an editable Word/Excel version so you can adjust minor inputs

Yes — our formats comply with RBI / bank norms and past approvals (we also provide a “CA review stamp” in pro plans).

We offer money-back guarantee or rework support (terms apply) — we stay with you until approval.

Typically 3 to 5 years forecasts. Professionals plan can include up to 7–10 years as needed.

End-to-end payments and financial management in a single solution. Meet the right platform to help realize.

CA Vikas Jain - Our Mentor