We mirror your general "What We Do" structure but specializing for MUDRA scheme.

The Pradhan Mantri MUDRA Yojana (PMMY) enables micro-credit

to non-farm, non-corporate

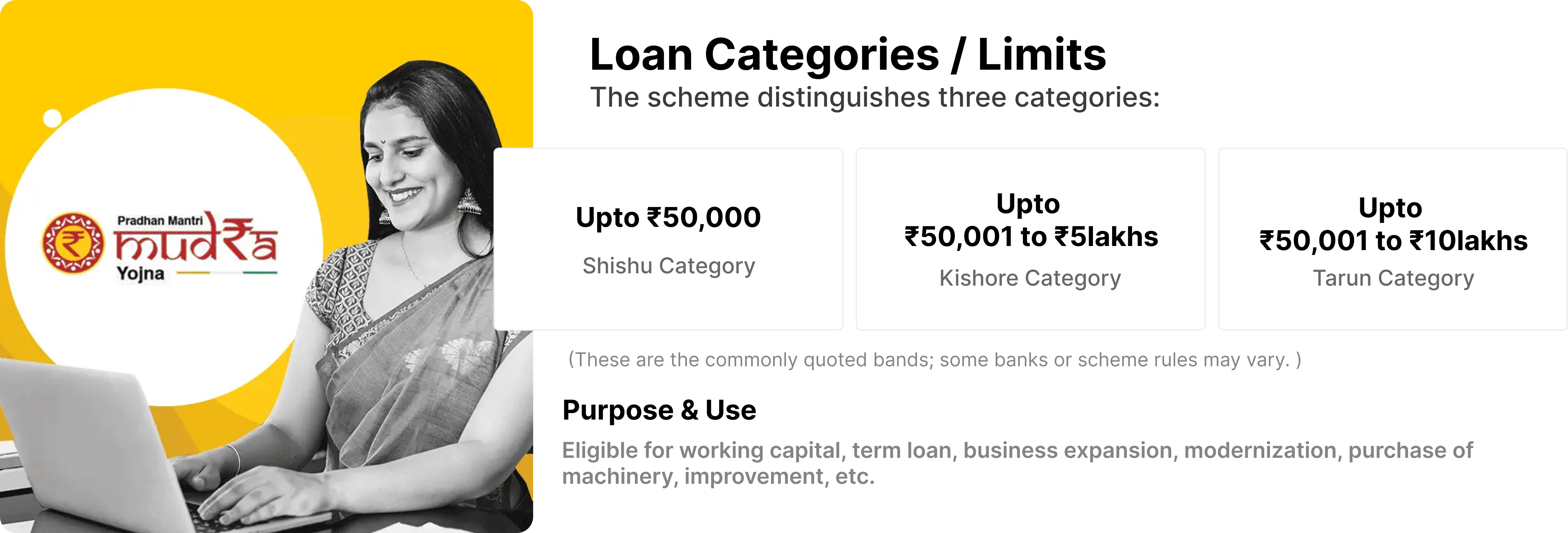

Pradhan Mantri MUDRA Yojana (PMMY) is a scheme set up by the Government of India (GoI) for providing Mudra Loans up to Rs. 20 lakhs to the non-corporate, non-farming small & micro enterprises. Mudra Loans are provided under four categories as mentioned below:

Upto ₹50,000

Shishu Category

₹50,001 to ₹5 lakhs

Kishore Category

₹5,00,001 to ₹10 lakhs

Tarun Category

₹10,00,001 to ₹20,00,000

Tarun+ Category

Mudra Loans are provided to income generation small & micro enterprises engaged in :

Trading

Manufacturing

Services Sector

Extended by Commercial Banks, MFIs, NBFCs and other financial intermediaries

Provides financial assistance to small and micro business to help them develop and expand their businesses.

Types of Eligible borrowers:

Individuals

Proprietary Concern

Partnership Firm

Public Company

Private Limited Company

Entities of any other legal form

The applicant should not be a defaulter to any bank or financial institution and should have a satisfaction credit track record.

The individual borrowers may be required to possess the necessary skills experience/knowledge to proposed activity.

The need for educational qualification, if any, need to be assessed based on the nature of the proposed activity, and its requirement.

Term Loan

Overdraft Limit

Working Capital Loan

Composite Loans for acquiring Capital Assets

Margin/Promoter’s Contribution is as per the policy framework of the lender, which is based on overall guidelines of RBI in this regard. Banks may not insist for margin for Shishu loans.

Interest rates are to be charged as per the policy decision of the bank. However, the interest rate charged to ultimate borrowers shall be reasonable.

First charge on all assets created out of the loan extended to the borrower and the assets which are directly associated with the business/project for which credit has been extended.

Tarun Plus: Covering loans above 10 lakh and upto 20 lakh for those entrepreneurs who have availed and successfully repaid previous loans under the ‘Tarun’ category.

Interest rates should be charged as per the lender’s policy. However, the interest rates charged to ultimate borrowers should be reasonable.

Answer few questions and get matched with best suitable scheme(s).

Provide basic details & documents and the advanced technologies would capture/auto-fill required details through smart analytics.

View offers from 200+ Lenders and get Digital Approval from selected bank.

Check the real time status of your application at your convenience.

For loans up to ₹5 lakh: maximum tenure around 5 years including moratorium of up to 6 months

For loans between ₹5 lakh to ₹10 lakh: maximum up to 7 years including moratorium period of up to 12 months.

Up to ₹50,000 (Shishu): typically no margin required.

₹50,001 to ₹10 lakh: margin may apply (e.g. 20%) depending on lender policies.

Collateral or security may be required as per bank & scheme norms, unless covered under guarantee schemes.

The scheme is supported by guarantee cover under a Central guarantee mechanism (e.g. via NCGTC / CGFMU) so that small borrowers can avail collateral-free credit to some extent.

Competitive interest rates as per bank norms + applicable taxes.

Processing / upfront fees: often nil for Shishu / Kishore in many banks; for Tarun could be ~0.50% (plus tax) (varies by bank).

Other scheme charges, guarantee fees, etc. may apply.

We provide weekly status updates and help close queries quickly.

No — sanction lies solely with the lending institution. We maximize your probability by preparing a strong proposal.

Many MUDRA loans, especially under Shishu, are covered by credit guarantee schemes (like CGFMU), making them collateral-free. However, the final requirement depends on the bank's policy and your profile.

PMMY is a credit (loan) scheme, not a subsidy scheme. While some MUDRA loans might be eligible for other government subsidies (like interest subvention), MUDRA itself is not a direct cash subsidy.

Almost all major Public Sector Banks (like SBI, PNB, BoB), Private Sector Banks (HDFC, ICICI, Axis), Regional Rural Banks (RRBs), and NBFCs/MFIs are eligible to lend under MUDRA.

The PMMY scheme generally covers loans up to ₹10 lakh (or ₹20 lakh for Tarun+). For higher amounts, we would assess your needs and file under other suitable schemes like Stand-Up India or general MSME loans.

End-to-end payments and financial management in a single solution. Meet the right platform to help realize.

Accountant

A local retailer struggled with cash flow management and tax compliance. With Financesewa's accounting guidance, they streamlined bookkeeping, reduced tax liability, and improved profit margins by 30% within a year.

Entrepreneur

Financesewa helped us improve our financial planning and grow our revenue efficiently within months of consulting.

Business Owner

With Financesewa’s expert support, we managed to expand operations efficiently and stay fully compliant.

Consultant

Their tax strategy advice was spot-on — we’ve saved so much time and money thanks to their expert advice.

CA Vikas Jain - Our Mentor